Voltas rides the summer wave. But is the stock still a cool bet?

Source: Live Mint

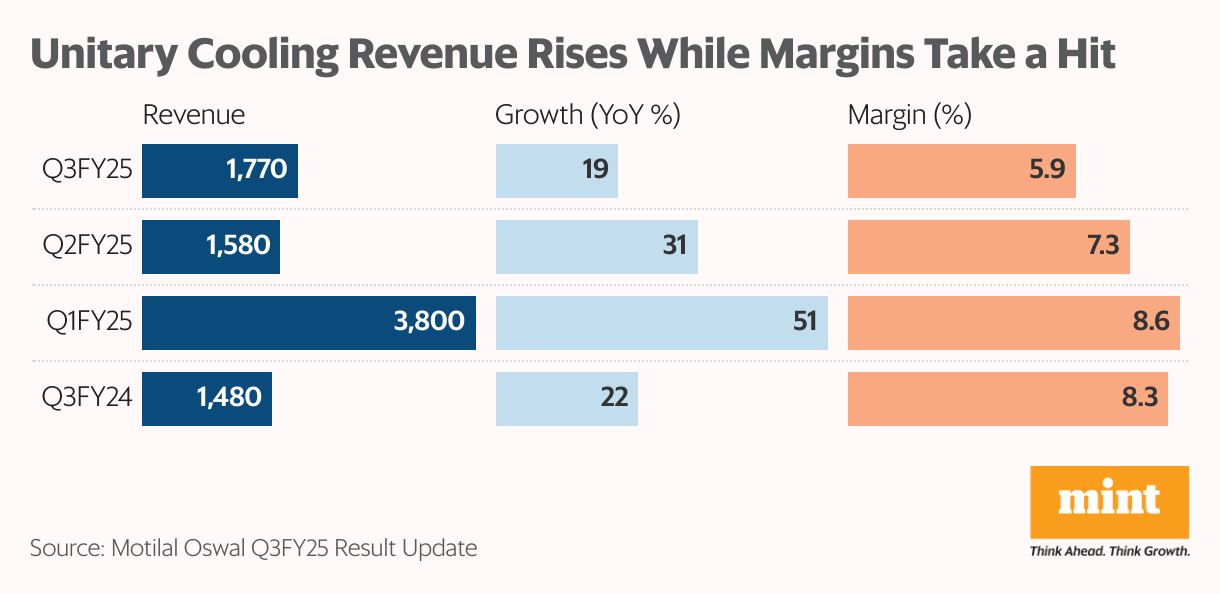

As a result, Voltas, the leading air conditioner brand, expects stronger sales momentum. But how well is the company positioned to capitalize on this opportunity? Before unpacking the story, let’s take a look at its Q3FY25 performance:

Unitary cooling products lead Voltas sales

Voltas’ business comprises three business segments, including unitary cooling, which markets cooling products such as room air conditioners, air and water coolers, and commercial refrigeration products.

The unitary cooling segment generated 68% of Voltas‘ total revenue in the first nine months of FY25. Electro-mechanical Projects and Engineering Products contributed 29% and 4%, respectively. Our focus in this story is the Unitary Cooling segments.

Room ACs drive growth, commercial refrigeration lags

Within unitary cooling, room ACs (RAC) continue to be the key growth driver. In Q3FY25, 60% of total sales in the unitary cooling segment came from room ACs, while 15% came from commercial refrigeration, 5% from air coolers and the remaining 20% from others.

Voltas RAC continues to lead the industry by maintaining its growth momentum, with volume growth of 42% in 9MFY25. It remains the market leader in split and window AC, with an exit market share of 20.5% in December 2024. The company reversed a three-year market share decline, strengthening its performance.

On the other hand, the commercial refrigeration (CR) segment faced some challenges. Lower customer capital expenditure dampened demand, prompting Voltas to clear inventory through promotions, impacting margins.

In contrast, the air cooler segment performed strongly despite seasonal weakness in the third quarter, with 80-85% YoY volume growth in 9MFY25. Voltas’s market share in air coolers reached 11.1% in September 2024, making it the No. 2 brand after Symphony.

Quantity tie-ups with distributors and sub-dealer schemes contributed to the air cooler’s strong performance. Voltas aims to maintain the product growth rate with volume growth of 70-80% (YoY) in the coming years.

Further, demand for commercial ACs remained strong, with 12-15% annual growth in Q9FY25, and similar growth is expected going forward.

Margin pressure dampens revenue growth

Note that the third quarter remains a seasonally weak quarter for cooling products. Despite that, the segment recorded strong revenue growth of 20% year-on-year (YoY) to ₹1,771 crore, led by RACs, air coolers and commercial ACs.

However, the strong revenue growth was dampened by lower earnings before interest and tax (Ebit). Headwinds in commercial refrigeration, operating deleverage from lower utilisation at the new AC facility in Chennai, and higher marketing expenses impacted Ebit, which was further aggravated by higher commodity costs and rupee depreciation.

As a result, margins fell to an over four-year low of 5.9% from 8.3% in Q3FY24. However, the company is still not keen on improving margins. Instead, it prioritises market share through volume growth over price hikes, unlike peers who have taken 1-2% hikes to protect margins and profitability. Due to this, ICICI Securities expects Voltas’s margins to fall further by 1% in Q4.

Also Read : Bitcoin bottom forming as Fed eases, Trump softens on tariffs: Analyst

Strong summer demand to boost Voltas sales

The demand for RACs is expected to increase significantly in the coming months due to expectations of a scorching summer season with above-normal heat waves across the country.

As a leading company, Voltas is witnessing strong demand for its RACs with the onset of summers across India. Notably, in FY24, Voltas’s AC sales grew 35% to over 20 lakh units—its highest-ever AC sales, making it the first company to cross this milestone.

The momentum continued in FY25 with Voltas’ volumes growing 35% during the April 2024-January 2025 period, outperforming the industry’s growth of 30%. With demand expected to surge in the coming months, Voltas expects to maintain its lead in volume growth, surpassing the industry’s expected growth of 30%.

Also Read: Voltas’ fortune tied to AC business despite Voltbek optimism

Capacity expansion and cost optimisation to fuel growth

To capitalise on demand, the company is holding off price hikes despite increasing production costs, unlike peers who have taken 1-2% hikes to protect margin. This cost advantage strengthens Voltas’ position in the mass market, supporting its volume growth and reinforcing its leadership in the segment.

In addition, Voltas plans new seasonal launches across categories, which will help it gain market share. Moreover, the company is also optimising costs to balance profitability and maintain margins at the current level without price hikes.

Further, Voltas has set up a new manufacturing facility in Chennai with a capital expenditure of around ₹400 crore to capitalise on the strong demand. This facility operates at 40-50% capacity and is expected to reach utilisation by FY26 as demand increases.

With its other facility running at full capacity, Voltas’ profitability and margin improvement depend on operational efficiency at this facility. As this facility utilisation improves, Voltas’ margins and profitability will strengthen. Additionally, PLI incentives from the facility are expected to be received from Q1FY26, helping it boost profit and margin.

Declining compressor imports from China a concern

Concerns over compressor import from China remain as the government has not renewed BIS licenses for several China-owned entities. The domestic capacity meets only 40-45% of the annual compressor demand, while the rest is imported. Thus, the non-renewal of licenses affected the supply of compressors, which would have impacted Voltas.

However, the company has managed to ease the supply by sourcing from alternate sources for the current season. Now, the company focuses on in-house compressor manufacturing to make supplies more reliable. It has announced a capital expenditure of ₹260 crore for the purpose under PLI 3.0.

Also Read: Hot summer forecast to boost consumer durables, beverage sales in India

What financials say, and where valuation stands

Volta’s consolidated revenue grew 28.6% YoY to ₹10,645 crore in Q9FY25, led by a robust 37.6% growth in the cooling business and 16.8% growth in electro-mechanical.

On the other hand, Voltas’ Ebitda margin grew 3.9% YoY to 7.4% in Q9FY25, led by a 27.7% margin in engineering products, despite poor margins in the cooling business. This led to a massive 335% rise in net profit to ₹599 crore, albeit on a weak base.

The company trades at a price-to-equity valuation of 67, 60% premium to its 10-year median multiple of 42. Relatively, it trades at a discount to Blue Star (80) and Johnson Control Hitachi (94).

Voltas’ current valuation appears to be full, and a lot depends on its performance in the much-awaited summer season. Moreover, Voltas may continue to trade at a valuation discount to peers due to their stronger growth rates.

Nonetheless, Voltas remains a strong play on rising RAC penetration, backed by its market leadership, strong brand presence, and extensive reach across India.

Motilal Oswal expects Volta’s revenue, Ebitda, and profit to grow at 12%, 20%, and 23% annual growth rates during F25-27. It assigns a target price of ₹1,710, 20% higher than the current price of ₹1,430.

For more such analyses, read Profit Pulse.

Madhvendra has been a passionate follower of the equity market for over seven years and a seasoned financial content writer. He loves reading and sharing his opinions about publicly listed Indian companies and macroeconomic trends.

Disclosure: The writer does not hold the stocks discussed in this article. The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.