Trump 2.0: How to make your portfolio great again

Source: Live Mint

—Donald Trump, The Art of the Deal

Some have called it the ‘greatest political comeback of all time’. Others labelled it as the world’s most extreme ‘reality television show’. Donald Trump’s crushing victory in the US presidential elections has elicited a range of responses, from giddy delight to soul-crushing despair. But for global financial markets, the ‘Trump trade’ only fuelled a furious rally, with Wall Street and other major stock indices vaulting to record highs in tandem with Bitcoin, while the US dollar strengthened, and bond yields jumped sharply in the immediate aftermath of the election results.

However, the risk-on sentiment petered out the very next session as the initial euphoria cooled off and markets began digesting what Trump 2.0 could mean for equities, treasuries and the global economy.

Dalal Street too witnessed a similar arc—the Nifty jumped 1.1% on 6 November but gave up all the gains the next day.

For a market as domestically driven as India, focusing on US elections seems an excessive exercise in futility. Watching the feverish discourse over ‘MAGA’ (make America great again) and ‘wokeism’ might be an endless source of dopamine hits, but are those issues really relevant to domestic investors?

The instinctive answer may be ‘no’, but as many veteran market watchers argue, the deeply interconnected nature of markets coupled with Trump’s loose-cannon approach to policymaking means India cannot be immune to global upheavals, be it geopolitical or financial.

Not to mention the tectonic shifts underway in various sectors, which call for a more hands-on approach on the part of investors as Trump’s second innings gets underway.

Acche din: IT edition

Trump’s major economic policy promises in this election were a blanket increase in tariffs (with additional levies on Chinese imports), lower corporate and individual taxes, and tightening of immigration.

There’s often a wide gulf between campaign rhetoric and policy implementation. Even then, decoding Trump’s policy statements is a job more suited to clairvoyants rather than macroeconomic forecasters.

“Assessment of the impact of Trump’s victory on Indian markets will be very premature at this stage. The markets are pre-empting at this point in time the probable policies to be adopted by the Trump administration based on the experience of his past tenure and the statements made during the election process,” Ajit Banerjee, president and chief investment officer of Shriram Life Insurance, told Mint.

That said, some domestic sectors are expected to gain from Trump’s stated policy stance.

The first is the Indian IT sector, which stands to benefit not only from higher US economic growth and the resultant increase in tech spending by American firms but also a stronger dollar.

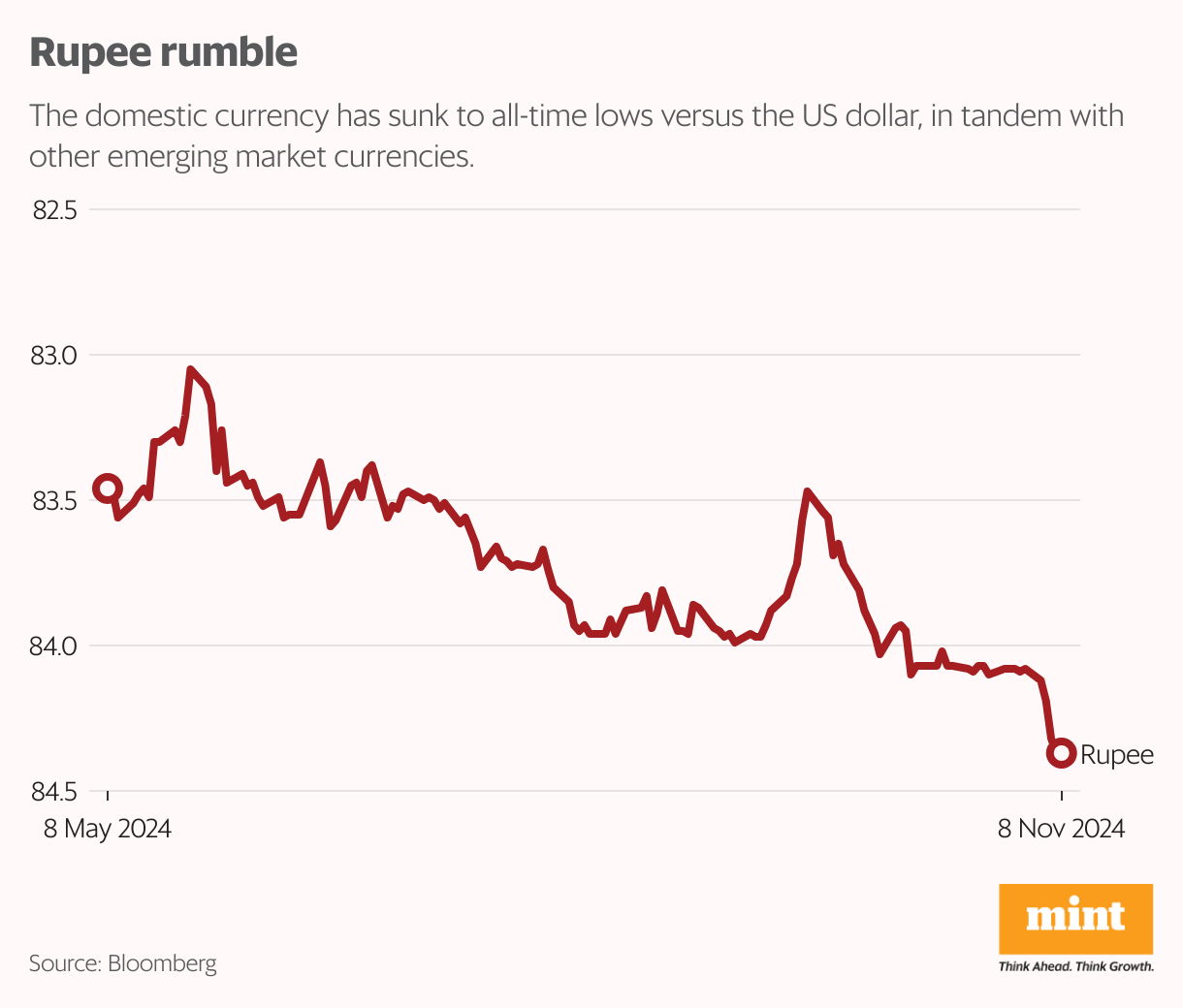

The US dollar soared to a four-month high on 6 November, weighing on most emerging market currencies, including the Indian rupee. The rupee has hit a new lifetime low of 84.37 against the greenback, with many analysts projecting it breaching the 85-mark soon. A depreciating rupee is a tailwind for exporters like Indian IT firms, which earn a significant portion of their revenue in dollars.

“With Trump back in power, corporations are expecting a lowering of the corporate tax rate. This would, in turn, boost discretionary spending by enterprises, which consequently may induce higher spending on IT projects,” Banerjee said.

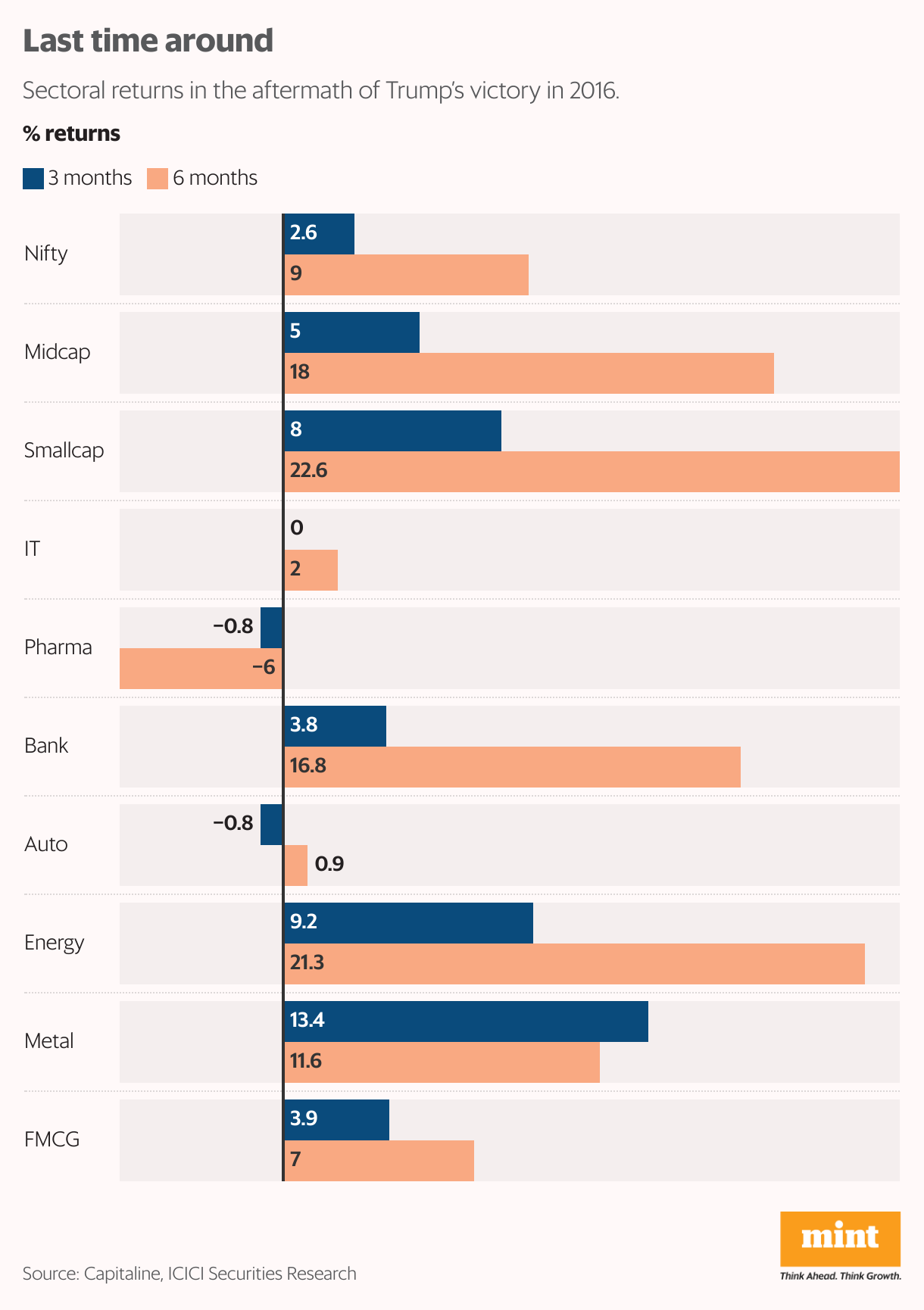

To recall, during Trump’s first presidency, the Nifty IT index went up by 150%.

“Indian IT firms are well-positioned to benefit from a potential rebound in US IT spending. Even recent Q2 results have indicated a positive trend in BFSI (banking financial services and insurance) spending in the US, which could be a strong growth driver for Indian IT companies,” he added.

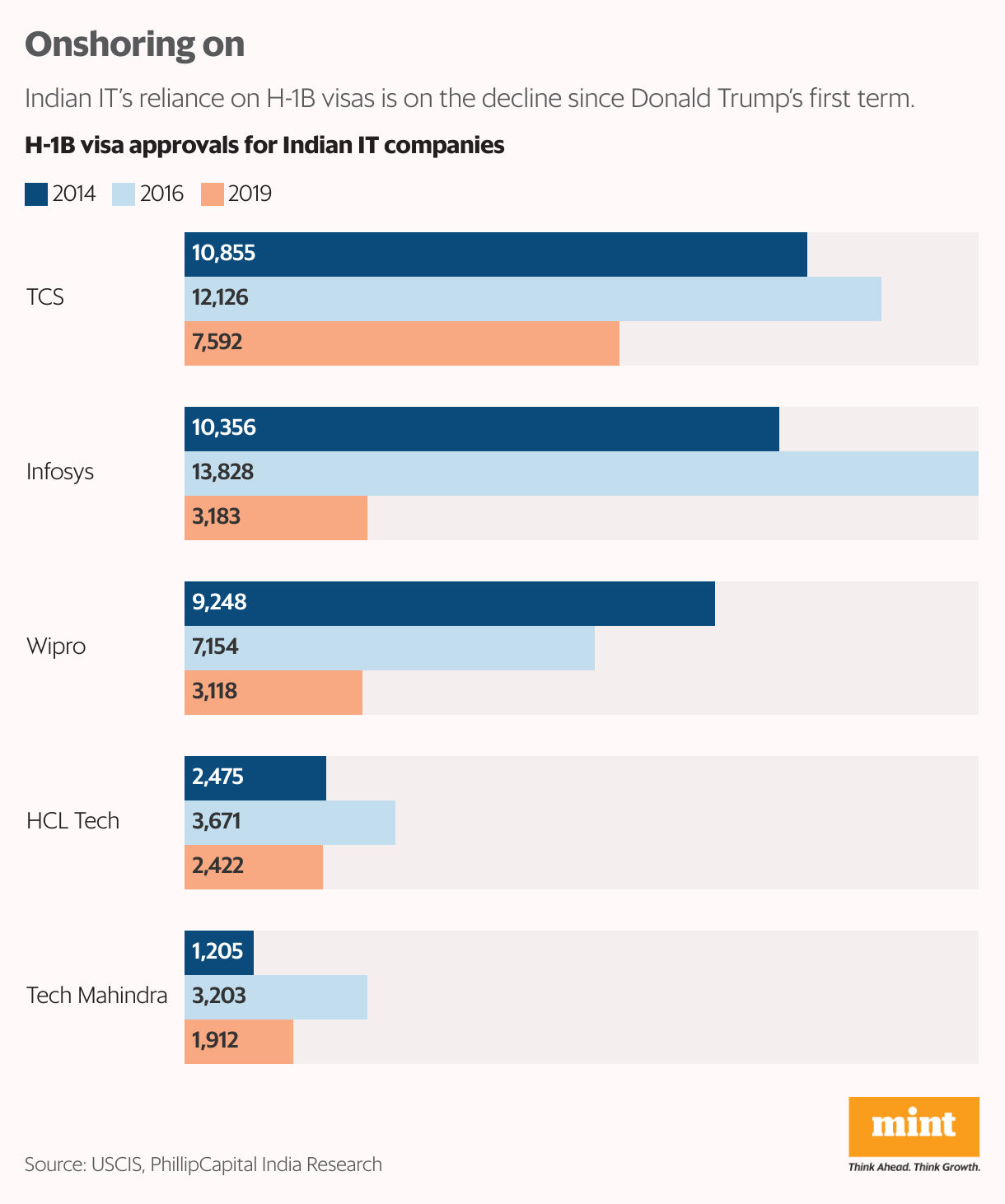

While the proposed tighter immigration norms may have an adverse impact on Indian IT majors to a certain extent, most of them have reduced their reliance on visas, offering them a significant degree of insulation from potential policy shifts.

Investors with a good memory (a rare breed, by the way) might remember that Trump, in his first term, increased restrictions on H-1B visas, leading to a huge spurt in denial rates, which impacted Indian IT services providers.

However, analysts maintain the situation is different today.

“Two-thirds of IT services players’ US resources were on H-1B/L-1 visas in FY17, as per our estimate. The ratio of visa-dependent/local resources has now likely flipped. This is reflected in a 50-80% drop in H-1B approved visas for Infosys/TCS/Wipro over FY15-24. That insulates players to a large extent from any spike in denial rates,” brokerage house JM Financial said in a recent report.

Similarly, while the new US government can enact a significant increase in wage obligation for H-1B visas, JM Financial’s analysis of select software roles indicates that average wages for H-1B resources today are around 25% above the prevailing wages.

“Claims of H-1B employees displacing US workers due to lower wages are therefore difficult to ascertain,” it added.

Not just that, Indian IT majors have stepped up hiring of locals in markets like the US, Mexico and Canada, as well as employed more sub-contractors (temporary staffers who are already based on-site with valid visas). In any case, Trump’s ire is directed more towards illegal immigrants, whom he has threatened to deport.

Indian nationals received the highest number of work visas (H-1Bs) in the US, accounting for over 72% of the visas issued in FY23. The latest naturalization statistics (FY23) from the US show India ranks second after Mexico.

Sectoral winners-II

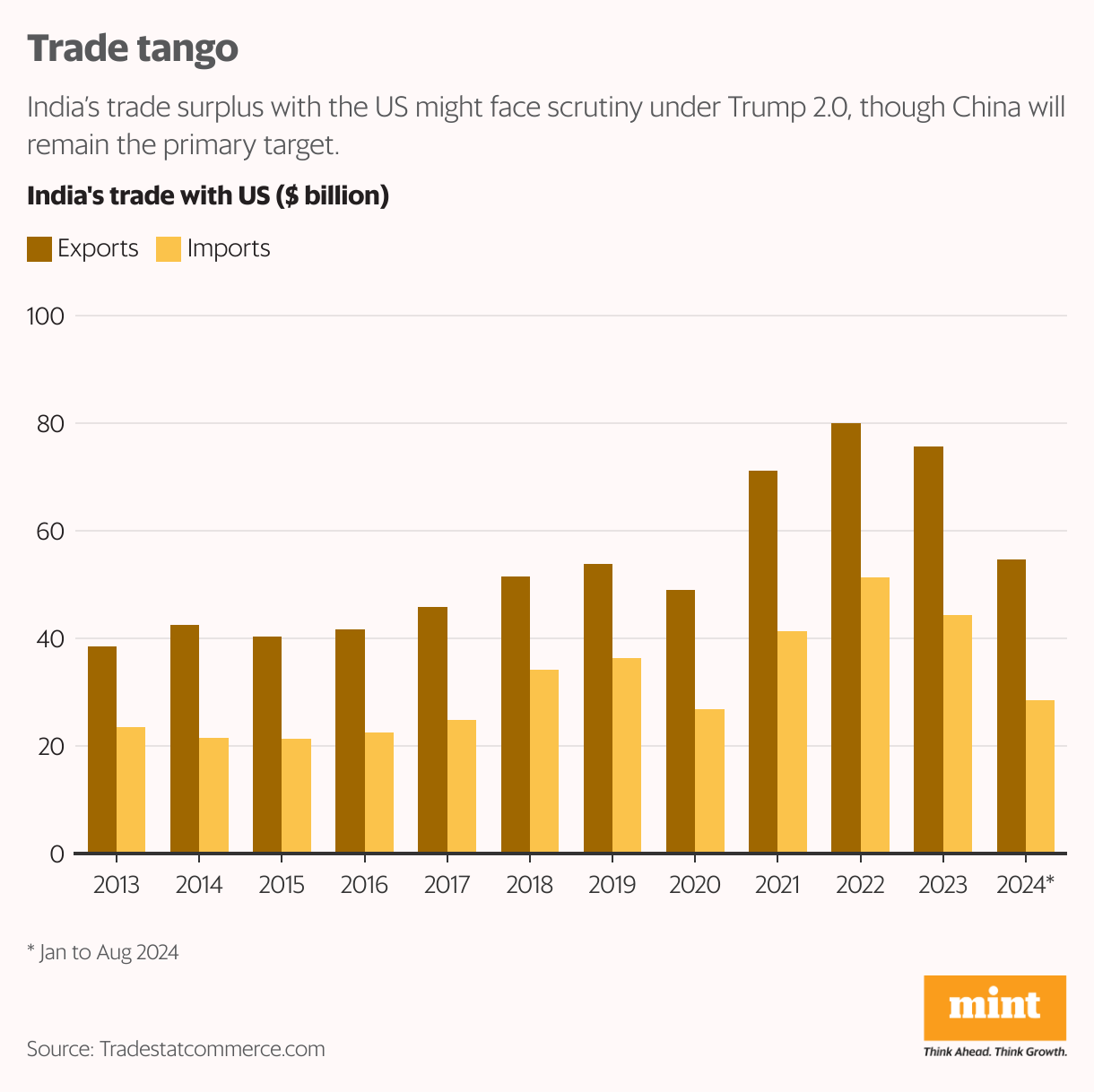

Trump has proposed a blanket increase in tariffs, but more so for imports from the US’ ‘enemy number one’—China. This theme can benefit Indian exporters, but only up to an extent, as the mercurial president-elect has the propensity to indulge in frequent (and public) trade skirmishes with friends and foes alike.

It is worth noting that Trump had characterized India as a “tariff king” and “trade abuser” during his campaign and vowed to increase levies on Indian goods. That said, his personal equation with Prime Minister Narendra Modi, and the prioritization of tightening the screws on China, can translate into a significant window of opportunity for Indian companies.

The US accounts for around 18% of India’s merchandise exports. The biggest export items include electronics, pearls and precious stones, pharmaceuticals, nuclear reactors, petroleum products, iron and steel, auto components and textiles.

Lowering the cost of medicines is on Trump’s agenda, while the Biosecure Act—which prohibits US federal agencies from procuring from “biotechnology companies of concern” (i.e. Chinese firms)—has bipartisan support.

Indian contract development and manufacturing organizations (CDMOs) stand to gain in this scenario, provided they strengthen their processes to ensure the safety and efficacy of their products.

Similarly, the acceleration of ‘China+1’ de-risking strategy can provide an impetus to Indian auto ancillary companies in terms of higher exports. The outgoing Biden administration has already implemented substantial hikes on Chinese auto imports, including a 100% tariff on electric vehicles (EVs), a 25% tariff on lithium-ion EV batteries and a 50% tariff on photovoltaic solar cells.

")

View Full Image

“However, protectionist policies by Trump might require Indian companies to invest in the US to localize supplies, which were otherwise exported from India,” JM Financial said in a report dated 7 November. It added that commodities witnessed steep tariffs in Trump’s previous tenure, effectively disrupting efficient price discovery. With regionalism and ring-fencing in commodities picking pace, metal prices could inch up under a Trump regime.

Higher tariffs on Chinese imports can also result in higher competitiveness of Indian chemicals exporters as well as solar PV cells manufacturers.

In 2022, President Joe Biden extended the tariffs on solar imports imposed by Trump in his first administration. Some manufacturers in Southeast Asian nations like Thailand, Malaysia, Cambodia and Vietnam were also slapped with new duties as China was using their factories to dodge the US tariffs. That apart, a 50% tariff on semiconductors made in China will go into effect in 2025.

Export of Indian solar modules to the US grew from ₹600 crore in FY21 to ₹10,500 crore in FY24.

Expect higher collaboration with India on security issues in the Indo Pacific region… this should benefit the defence sector.

— Elara Capital

Another major sector which analysts have their eyes on is defence. India’s role as a counterweight to China has been a policy fulcrum for successive US administrations, be it Democrats or Republicans. Trump’s fire-and-brimstone approach towards Beijing will only deepen this engagement, potentially leading to more deals in the defence sector.

“Generally, expect higher collaboration with India on security issues in the Indo- Pacific region, which would propel greater partnership in defence engagements. This should benefit the defence sector,” analysts at Elara Capital said in a note.

“We expect high tech sectors such as AI, semiconductors and EMS (electronic manufacturing services) to continue to be in favour as diversification of supply chains remains aggressive amid rising investments in AI (recall Nvidia-Reliance collaboration),” they added.

On a macro level, Trump’s vocal support for the American oil and gas sector can lead to a significant increase in production, which can keep global crude oil prices in check. This bodes well for both Indian refiners and the country, with India’s import dependence on crude oil rising to an all-time high of 87.7% in 2023-24.

Enter the dragon

As anyone with even a rudimentary exposure to Bollywood can attest, sometimes the biggest hurdle in a blossoming romance is the entry of a third party. Those tingling with excitement at the prospect of a flaming (financial market) affair between India and the US during Trump 2.0 should note the third party in this equation—China.

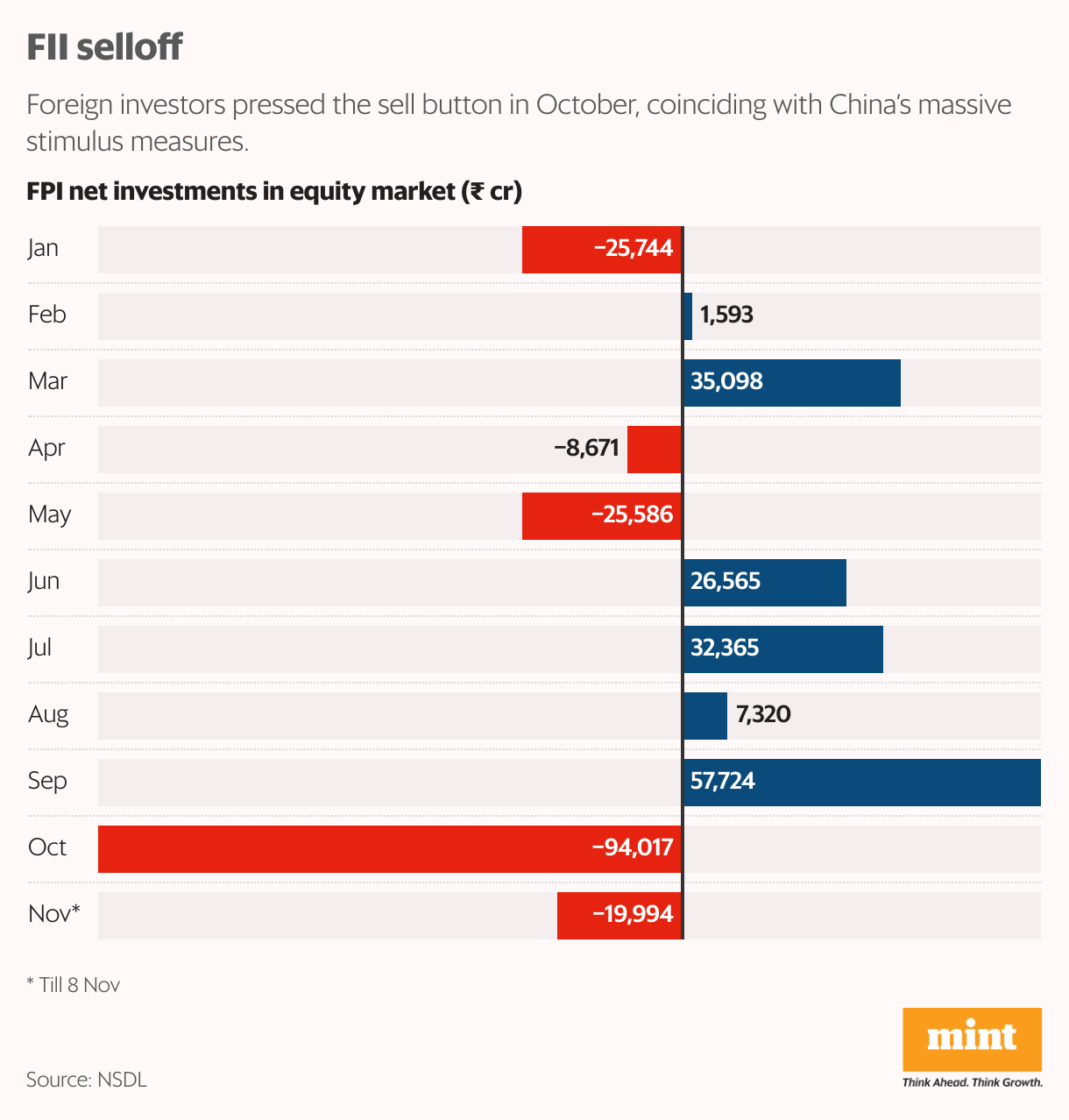

Foreign investors have piled into Chinese markets over the past few months as Beijing unveiled a raft of measures to support its faltering property market and stoke domestic demand.

Continuing with its stimulus measures, China on 8 November approved a humongous $1.7 trillion package aimed at bolstering cash-strapped local governments and shoring up consumer demand. The growing attractiveness of China has led to massive outflows from other emerging markets, including India.

Foreign investors pulled out a record ₹94,000 crore ($11.2 billion) from the Indian stock market in October, followed by around ₹20,000 crore ($2.3 billion) in November so far.

With Trump’s corporate tax cuts and fiscal expansion measures expected to boost US growth, many analysts say emerging markets are even less likely to find favour with asset allocators, especially in light of likely worsening in global geopolitics and trade.

“FPI (foreign portfolio investment) outflows from India may accelerate in the near term, given the dominance of passive inflows in FPI flows…. any large fiscal stimulus from China to offset the negatives of higher US tariffs on Chinese imports could be a further negative for FPI flows into India,” Kotak Institutional Equities warned in a note.

That said, the rising heft of domestic institutional investors means Indian markets are no longer hostage to FPI mood swings.

“We should also remember that China’s exports to the US were to the tune of over $500 billion in 2023. In contrast, China’s imports from the US stood at $165 billion or so. It is very clear where Trump’s priorities would lie. Also, Donald Trump is pro-business; he wants reciprocity from his trading partners, be it China, India or any other country. In that sense, as long as we get our bilateral trade deals right, Indian exporters should not worry about extra tariffs on Indian goods,” Kranthi Bathini, director of equity at WealthMills Securities, told Mint.

As long as we get our bilateral trade deals right, Indian exporters should not worry about extra tariffs on Indian goods.

— Kranthi Bathini

Investors, therefore, should focus their energies on stock selection rather than get entangled in the American geopolitical checkerboard.

“Sectors like IT, EMS, pharma and defence are likely to be clear beneficiaries, but some of these counters have already run up a lot, so stock selection is paramount from now on,” Bathini said. “In the defence pack, for example, the expected deal wins offer better revenue visibility, while the recent 30-40% correction in some frontline names like HAL and Mazagon Dock offer an attractive entry point. However, investors should temper their expectations. While defence is still an attractive long-term play, investors can expect mid-teens returns at these prices and not multi-bagger type performance of the recent past,” he added.

This is a view that resonates with many market experts.

“The tailwinds for Indian sectors from Trump 2.0 must be viewed in light of the gradually weakening domestic earnings cycle given moderating consumption and delayed government spending for capital-intensive sectors. Data for companies that have announced results so far shows that more than 50% of the companies have seen earnings miss in Q2FY25 vs 40% in Q1FY25,” Elara Capital noted.

In other words, domestic problems largely require domestic solutions. There’s very little Trump, or any other occupant of the White House, can do in this scenario.