Simhavalokana 2024: Mr. Market’s 10 lessons in the year gone by

Source: Live Mint

In Sanskrit, the word for a tooth, a bird and a Brahmin is the same: Dwij. Literally translated, it means ‘twice-born’. Milk teeth give way to permanent teeth; a bird is born as an egg before it is born in its avian form and Brahmin is believed to be spiritually reborn after the thread ceremony.

Or take the word simhavalokana. As a lion walks in the jungle, he periodically stops and looks back at the path he traversed. This retrospective glance is called simhavalokana but at an abstract level, it means reviewing elapsed time. As an investor, this is my simhavalokana for the year, or for the listicle-minded, ten (+1) things that Mr. Market taught me in 2024.

Investing experience can be a liability

In a roaring bull market, having an investment memory can be a handicap. In two decades as a professional investor, one has lived through business and economic cycles, shenanigans of unscrupulous promoters or companies that have held promise but never delivered. I evaluated MakeMyTrip (MMYT) early in the year when the price was around $45 per share. I had assessed the company a few times over the past decade but had opted not to invest. What bothered me was that for over a decade, MMYT had reported negative Ebitda (earnings before interest, taxes, depreciation, and amortization) for all years except two. Irrational competition or weak consumer spending had proved to be the spanners in the works. In my internal note, under the head ‘credit where it is due’, I acknowledged the turnaround in operating performance but assigned more weightage to my memory of weak, inconsistent profits. A 25-year-old, without the baggage of the past, might have approached this differently. The stock is up over 130% for the year and when I narrated the story of this ‘miss’ to a friend, he sardonically replied: “Dumbledores don’t make money in bull markets.”

Pay attention to changing industry structure

Over the last few years, many industries in India have consolidated; from cement, airlines to telecom. If one is early to catch on to this change, there is multi-year money to be made by investing in the survivors and share-gainers. The causes for consolidation can be varied—operating losses for inefficient players, weak balance sheets or regulatory changes—but the resultant pricing power and improvement in return ratios are generally received warmly by investors. On the other hand, just because an industry is a duopoly does not guarantee handsome returns. Ask Boeing and Airbus.

Mean reversion is never automatic

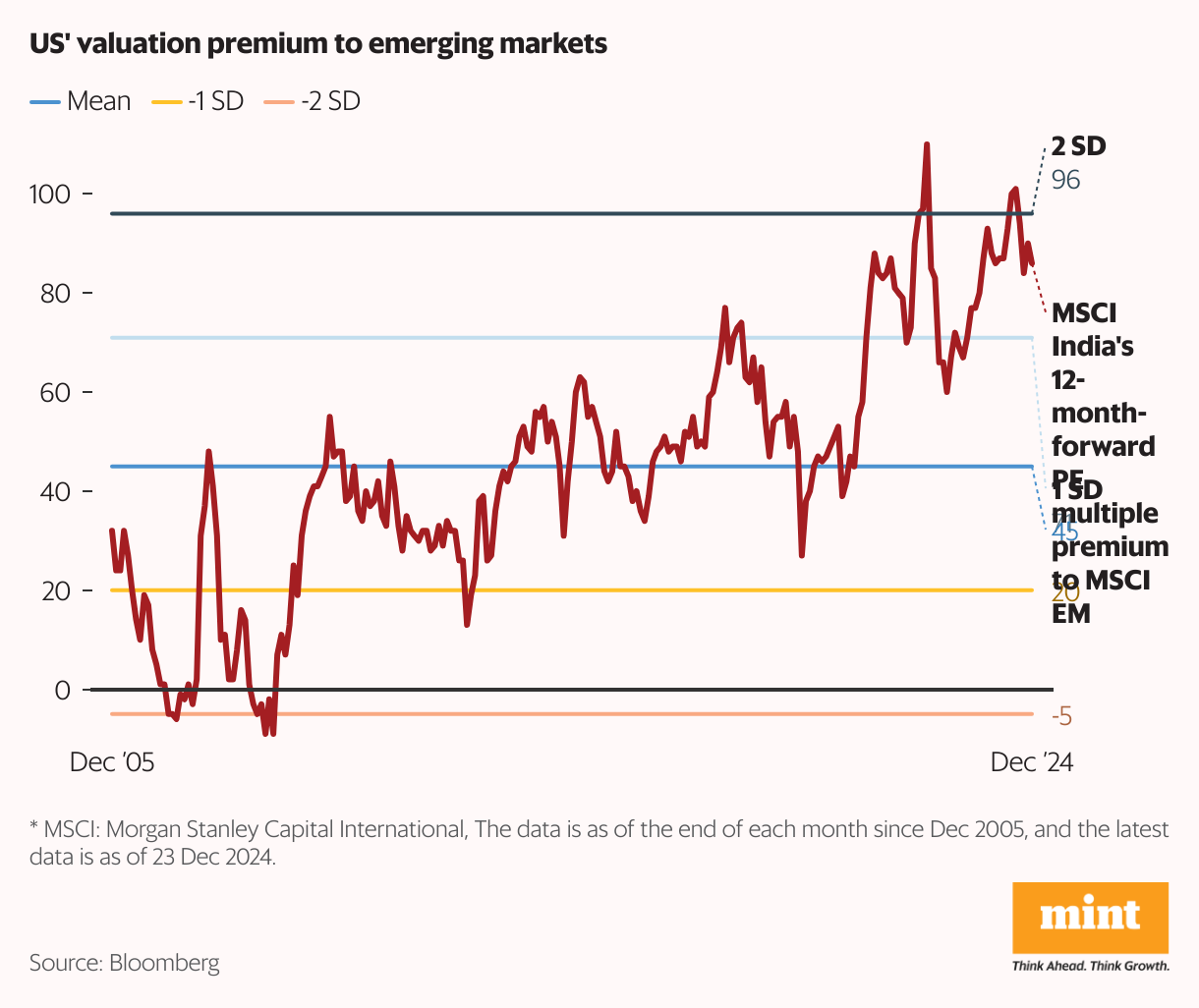

In the ‘risks’ section of their India reports, equity strategists have a chart showing the price-to-earnings (PE) premium of India over other emerging markets. At the beginning of 2024, this premium was quite elevated at 87% or about 1.5 standard deviations higher than the long-term average and the common refrain was that this metric has to mean revert i.e. the premium will shrink and head back towards the average. At the end of 2024, the premium is at the same level as the beginning of the year which means that the much-anticipated mean reversion has not happened. We have seen a starker expansion in the PE premium of the US markets to the rest of the world. Mean reversion does not happen mechanically; it needs a catalyst. Strong relative growth can lead to valuation premiums remaining elevated for a long time.

Climate change versus monetary policy

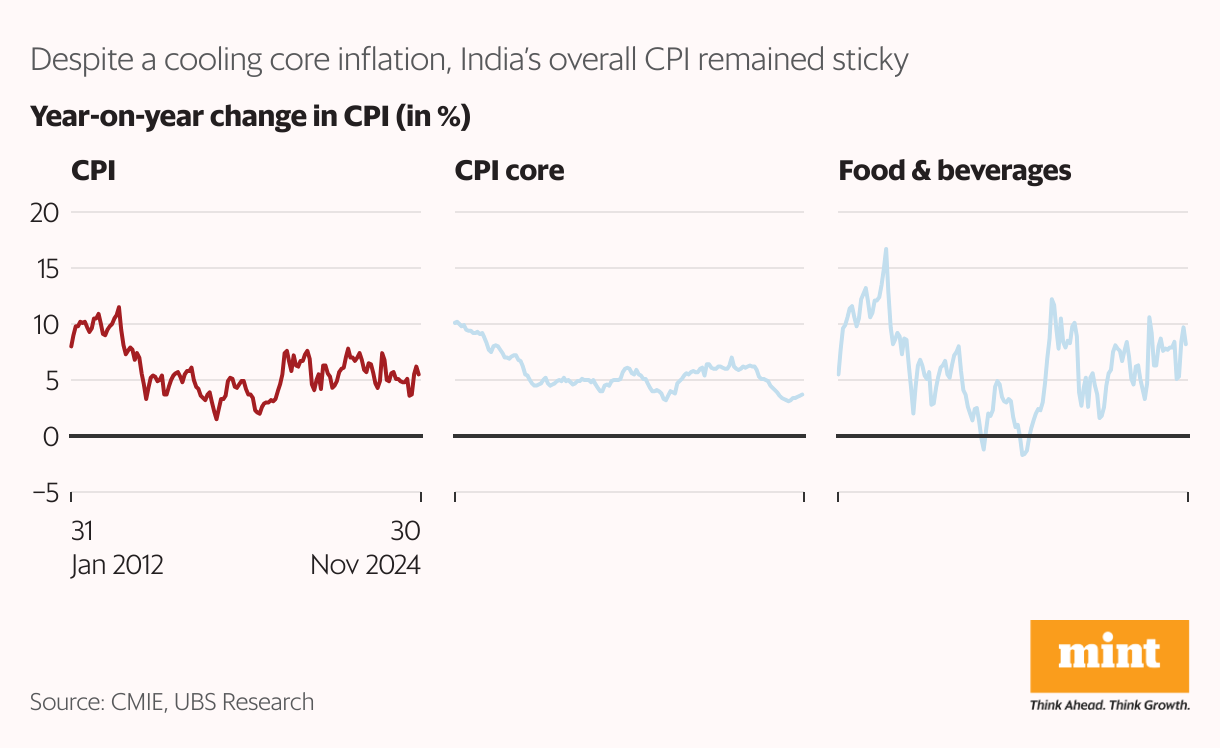

Many emerging market economists began the year with expectations of sizable interest rate cuts. Central Banks had hiked rates in the preceding few years, inflation was cooling off and markets were anticipating an easing cycle. But food inflation had different plans. Extreme weather events led to large, unanticipated spikes in food prices causing headline inflation to remain stickier than forecast. Given the chunky weightage of food in most emerging market inflation indices, this factor could not be brushed away. In India, too, we learnt a new term—tomato-onion-potato (TOP) inflation. And despite a cooling core inflation, the overall CPI remained sticky and we got no succour on rates. In a clash between climate change and a headline inflation-targeting monetary policy, the scales are tilted towards the former.

Instant gratification versus cold logic

During the pandemic, most families have had to shoulder a large, if not crippling, hospital bill for a loved one. This, I theorized, would create a strong demand for health and life insurance and companies selling these products would be beneficiaries of this trend. However, post FY22, the volume growth for such insurance products has barely been in the high-single digit. This defies logic but the reason for the tepid growth is possibly psychological. Consumers feel that they do not get anything in return for paying a sizable health or life insurance premium—no shiny new phone, no monthly SIP statement, not even a Insta-worthy vacation picture. The urge for instant gratification can sometimes defy the cold logic of risk mitigation.

Count your blessings

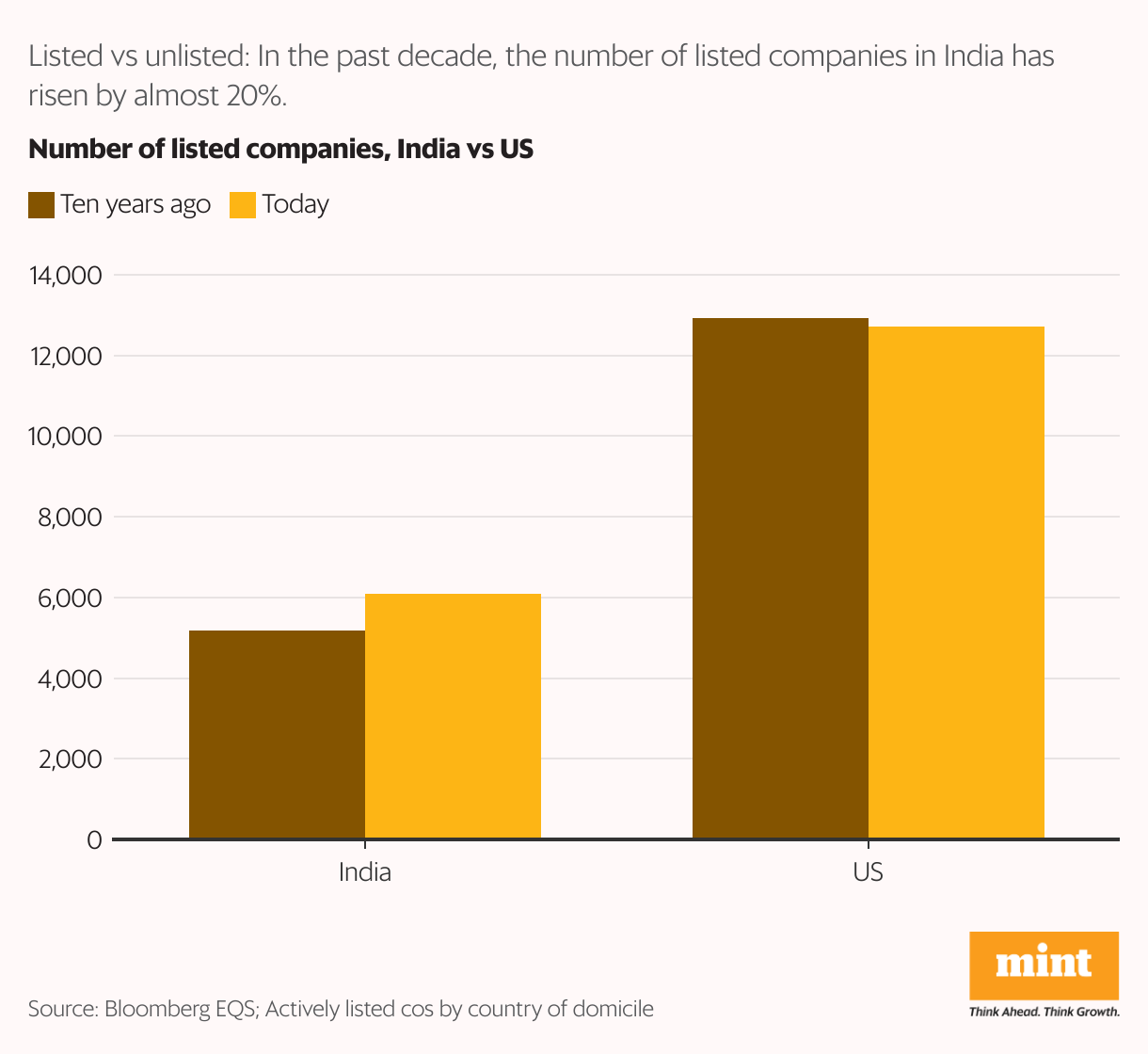

Taking your privileges for granted is human nature. It is only when you step back and broaden your gaze that you learn to count the blessings. A statistic that has confounded me, is that despite being the shining light of capitalism, the number of listed companies in the US has steadily dwindled. Staying or going private may be a consequence of massive amounts of private capital that chases US companies. In India though, it’s a blessing for the public market investor that startups aspire to be listed. This is borne out by the fact that the number of listed companies in India has gone up by almost 20% over the past decade. Also, for every one listed company with over half a billion dollars of revenue, there are almost two in the unlisted space. The combination of listing aspirations and a large reservoir of reasonably-sized corporates can only bode well for the future depth and breadth of public markets.

Look for bad macro news

Argentina. Pakistan. Sri Lanka. China. What’s common to all these countries? Of late, you have probably read only bad macro and political news about all of them. Yet, even after adjusting for local currency depreciation, their stock market indices have done exceedingly well in 2024. Even Germany, which seemed to be at the epicentre of all that was going wrong for Europe had its benchmark DAX index climb to an all-time high in December. If dire news about a country has been making the headlines for a while, odds are that the markets have already bottomed.

Do not fixate on events

Investors tend to fixate on the outcomes of events like an important election or a monetary policy meeting. There is a strong itch to rejig your portfolio in anticipation of what you think will be the outcome. This is a mug’s game because for you to make money from an event, you have to get two things simultaneously right: the outcome of the event and more importantly, the market reaction to that outcome.

Let’s assume that on the eve of India’s general election results you had the clairvoyance of seeing 240 seats for the Bharatiya Janata Party. The portfolio tinkering itch would have made you sell down your holdings or buy large amounts of portfolio protection or add defensive consumer staples names. That would have meant that you lost out on over 15% NIFTY returns in the next three months or your portfolio was saddled with what proved to be the worst-performing sector for the rest of the year.

Beware the IPO

Of late, India has seen a spate of IPOs—263 to be precise—since April 2019. An IPO, especially with a strategic investor or promoter selling stake, is a lopsided transaction. In effect, it matches up a very knowledgeable and motivated seller with an almost naïve buyer. Data from IIFL Equities analyses the performance of IPOs that listed during the five years from April 2019 till March 2024 and concludes that on average, if you bought the newly listed shares on the day after listing, you underperformed the respective sectoral indices by over 1% and if the IPO involved a selling strategic investor, the underperformance widened to almost 5%. Simple message – on average, the bulk of an IPO’s outperformance is captured on listing day. Post that, it’s a hard grind. Also, it is worth noting that these middling performance numbers are despite the strong market uptrend of the past five years.

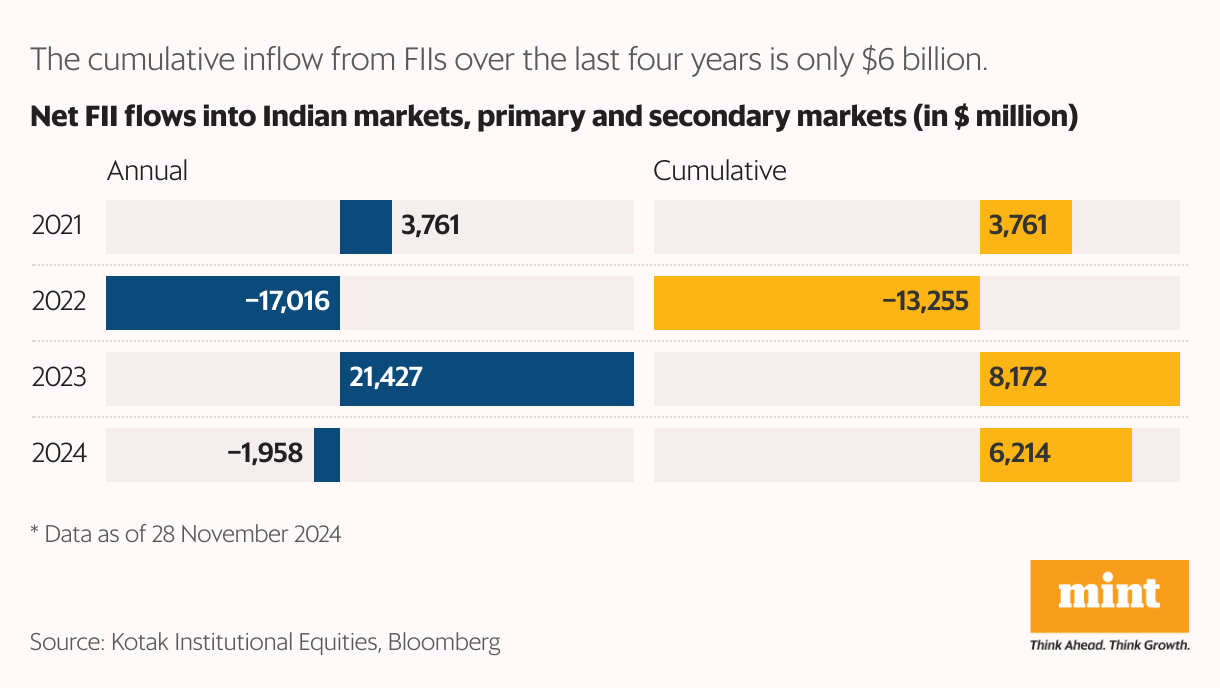

The FII flow obsession

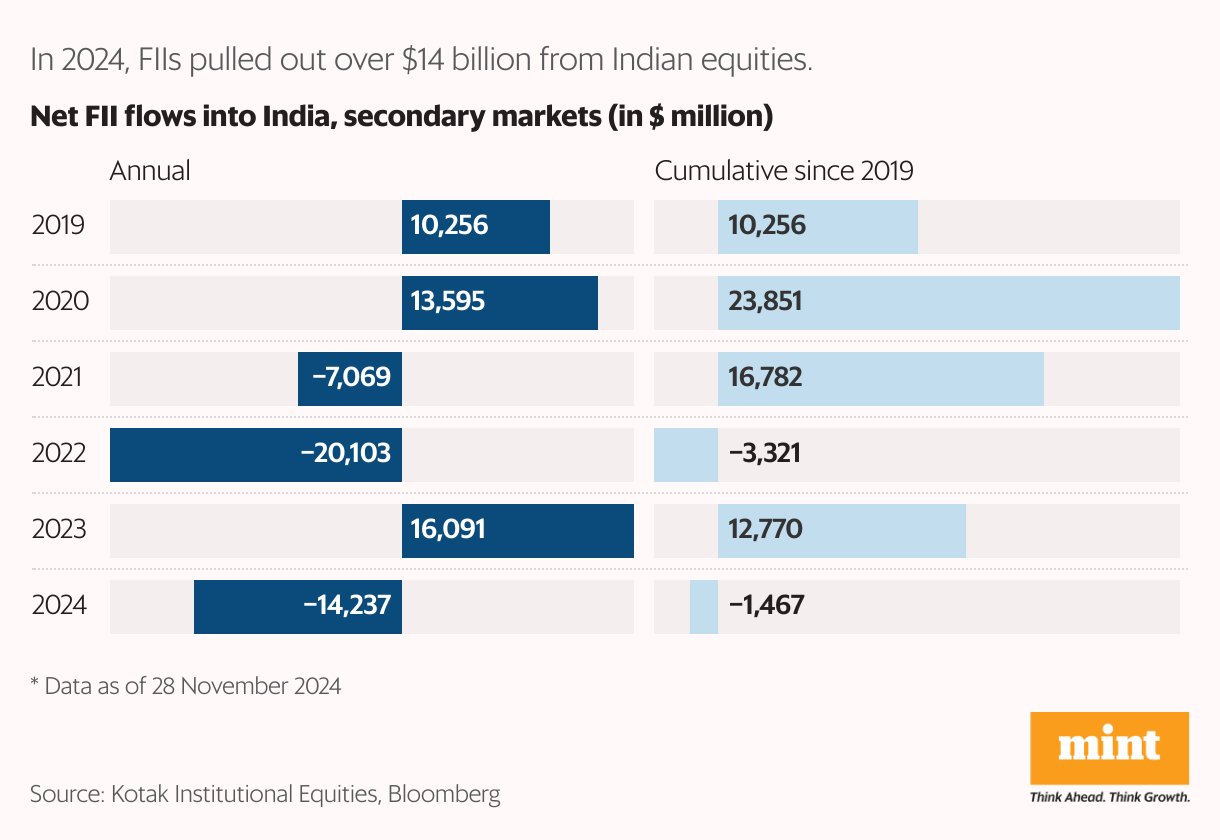

Foreign Institutional (FII) flows to India or the lack of them caused a lot of hand-wringing and theorizing in 2024. In fact, accounting for the YTD outflow of about $14 billion, FIIs have cumulatively invested nothing in the Indian secondary market since 2019. Even after considering their primary investments in IPOs, QIPs etc., the cumulative inflow over the last four years is only $6 billion or about two-three months’ worth of SIP inflows.

It is perplexing that this has happened in the backdrop of exceptionally strong earnings growth for corporate India, a stable macro setting and robust domestic flows leading to strong market performance. But to answer the frustrating question, “What do the FIIs want?”, it may be useful to step into the shoes of the global asset allocator.

The most important fact of her life in the last few years has been the upward march of US markets resulting in its unprecedented weight in the MSCI ACWI (67%) and MSCI World index (74%). These are the benchmarks that most global asset allocators are measured against. India, by comparison, has about 2% weight in both the indices. All across the globe, one can almost hear a whooshing sound of capital rushing back to the US. What FII asset allocators want, like all of us, is to keep their jobs and that leads to a behaviour that Charlie Munger observed: “Show me the incentive and I’ll show you the outcome.”

The man in the arena

Investing, at the end of the day, involves a leap of faith. Warren Buffett advises us to avoid leaping over 7-foot bars but to try and find 1-foot bars that you can easily cross over. But the fact that you will have to make a jump is unavoidable. Most times, you will be doing it amid a cacophony of unsolicited advice, the chatter of your inner fears or even relentless heckling. It’s only natural that sometimes you will end up making an investing mistake.

But when you feel downcast by errors or when the inner and outer din seems unbearable, I urge you to remember what Theodore Roosevelt said: “It is not the critic who counts: not the man who points out how the strong man stumbles or where the doer of deeds could have done better. The credit belongs to the man who is actually in the arena, whose face is marred by dust and sweat and blood, who strives valiantly, who errs and comes up short again and again, because there is no effort without error or shortcoming, but who knows the great enthusiasms, the great devotions, who spends himself in a worthy cause; who, at the best, knows, in the end, the triumph of high achievement, and who, at the worst, if he fails, at least he fails while daring greatly, so that his place shall never be with those cold and timid souls who knew neither victory nor defeat.”

Just the fact that you choose to be in this riveting arena of investing, is worthy of admiration.

Happy investing fellow travellers! I wish you a great 2025.

Swanand Kelkar is the managing partner at Breakout Capital Advisors. Views are personal.