New day, new high: Will stocks sustain Thursday’s momentum?

Source: Live Mint

Stock benchmarks touched new records and mid-cap stocks joined the Street party on Thursday, signalling rising risk appetite among investors betting on interest rate cuts in the US and earnings momentum in India.

The day witnessed a strong rally driven by a mix of factors: weekly derivatives expiry; a rate cut in China; optimism ahead of a rate cut that the European Central Bank announced later in the day; and hopes that the US Federal Reserve might follow suit soon.

On Thursday, the Nifty surged 1.9% to close at 25,388.90, while the Sensex rose 1.8% to 82,962.7, the highest percentage gain for both since 7 June. Both indices hit record highs during the day – Nifty at 25,433.35 and Sensex at 83,116.19. Meanwhile, the Nifty Midcap 100 climbed 1.2% to 59,640.30, reaching a record intra-day peak of 59,697.75.

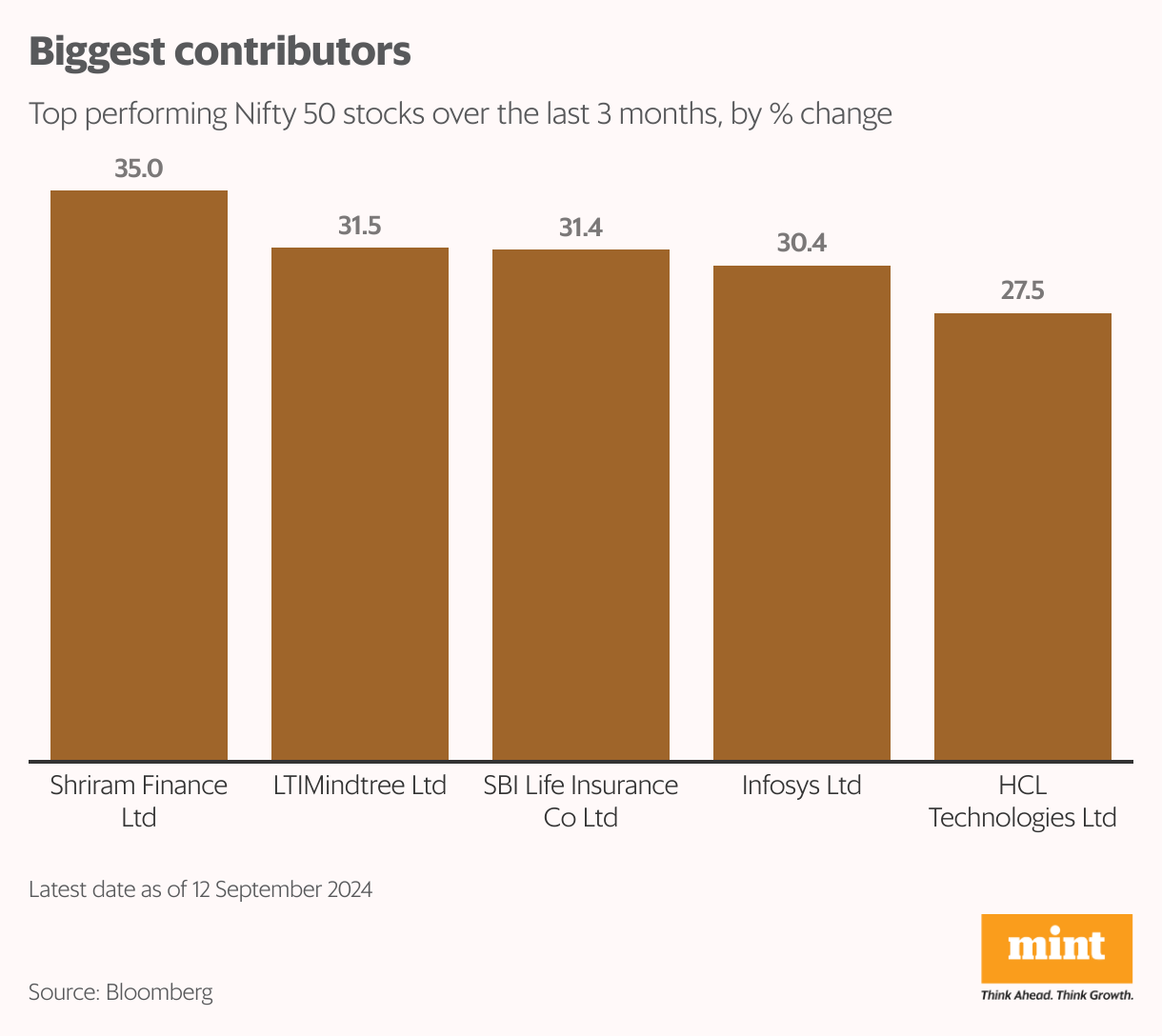

Besides sharp gains in Reliance Industries and banking stocks that boosted headline indices, the Nifty Metal index led sectoral performers with a 3% increase, followed by the Nifty Auto index with 2%.

Will rally sustain?

However, a crucial question emerges: Will the rally sustain or eventually fizzle out?

“Looks like the rally is all set to continue, with India becoming a go-to destination for foreign investors,” said Taher Badshah, CIO of Invesco Mutual Fund. However, he feels that India may now witness a more mature rally as rate cycle is expected to change, with some moderation in the industrials sector and increased interest in financials, technology, pharmaceuticals, and the consumption sectors, which were previously subdued by inflation, he explained.

Though Thursday’s surge was due to a combination of factors, Sandipan Roy, chief investment officer at Motilal Oswal Private Wealth expects the rally to continue, with occasional corrections along the way.

“Much depends on earnings growth and flows into Indian equities,” said Roy. He believes earnings momentum is expected to sustain, with the earnings of Nifty companies expanding at 13-14% compound annual growth rate in FY25 and FY26. Moreover, domestic institutional flows remain strong, while foreign flows could gain speed with potential rate cuts on the horizon, he said.

India’s political situation has stabilized after the general election, which is encouraging FIIs to consider long-term investments in the country, pointed out Vipul Bhowar, senior director, listed investments, Waterfield Advisors. “FIIs find undervalued top-tier stocks in the banking and financial sectors attractive. Additionally, new sectors and themes are currently raising capital through primary markets, generating significant interest from FIIs.”

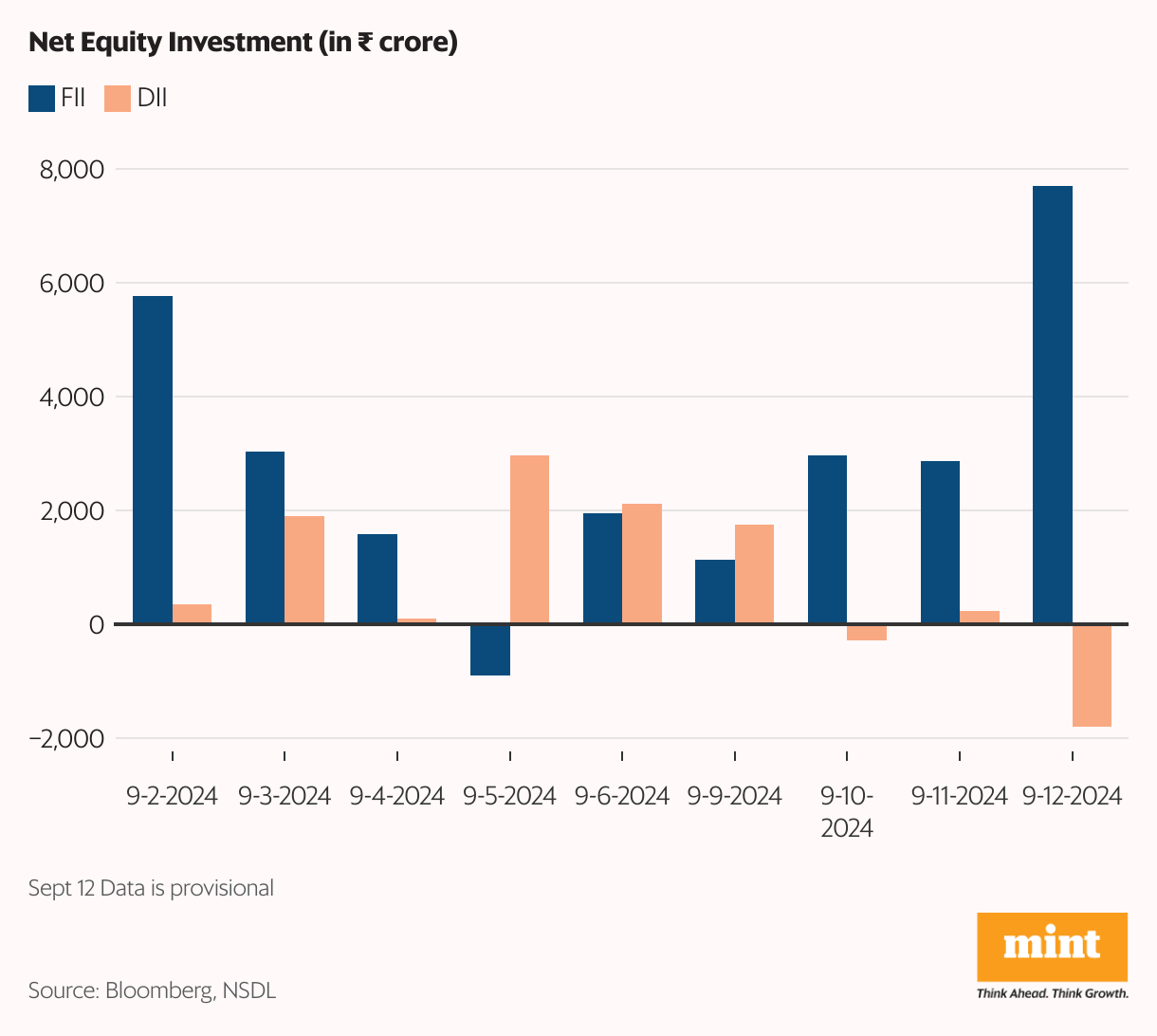

After selling equities worth ₹904.19 crore on 5 September, FIIs have been net buyers over the past five sessions. On Thursday, FIIs net purchased equities worth ₹7,695 crore, while DIIs sold equities worth ₹1,800.54 crore, provisional data showed.

According to Bhowar, positive economic indicators, expected rate cuts and the current under-ownership of Indian equities all suggest a potential rise in FII investments.

Dollar may weaken

While a rate cut by the US Fed seems imminent at next week’s policy meet, continued rate cuts over the next 6-9 months could weaken the dollar (as reflected in the dollar index) and raise allocations to emerging market equities in a risk-on environment, said Milind Muchhala, executive director at Julius Baer India. This could result in stronger FII inflows in the coming months, especially considering the extremely muted flows in the past couple of years, and considering the fact that India could now possibly see relatively higher allocation in the EM basket compared to the past, with its stronger growth prospects and relatively lesser conviction in China as an investable market.

The markets are already pricing in 25bps rate cut by the US Federal Reserve in the upcoming policy and 75bps across 2024.

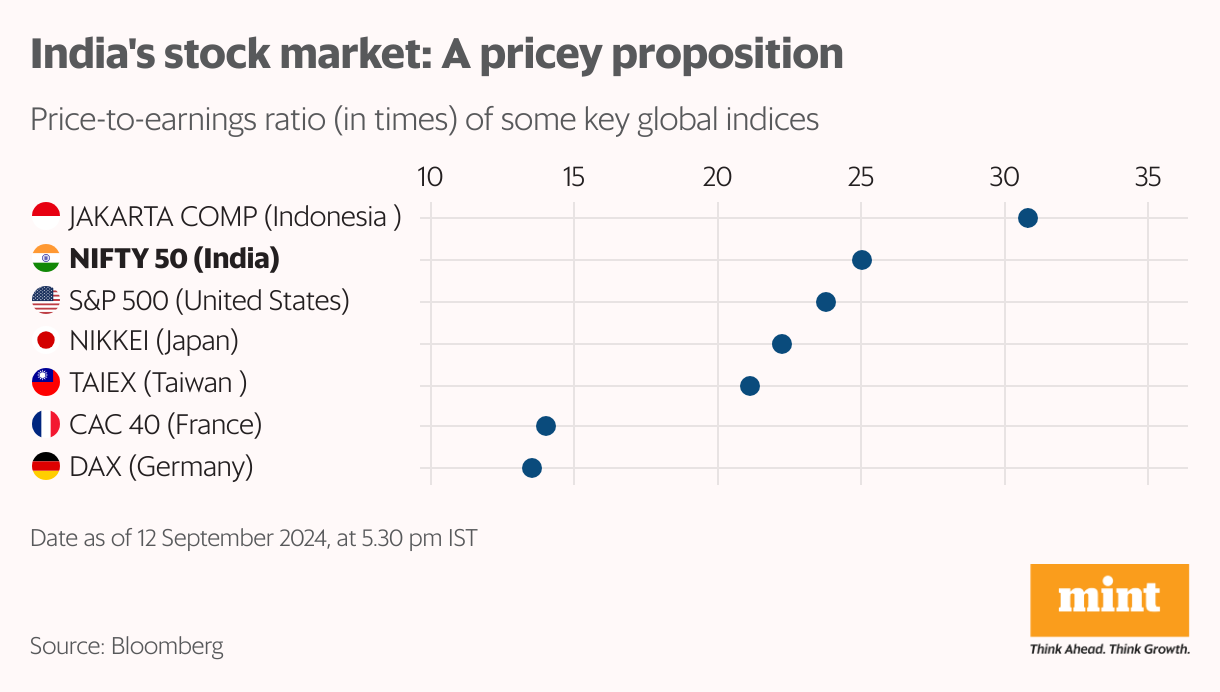

“However, if the Fed delivers slightly mixed/cautious commentary about its future rate cut path, it could slightly dampen investor sentiment in the near term,” said Muchhala. “Additionally, with the Indian equities having seen a healthy rally recently and currently trading at over 10% premium to its historical averages, any correction in the global markets or slowing down of corporate earnings momentum could result in a small drawdown in the markets, something that has been widely anticipated; however, the strong liquidity flows remains an upside risk to the markets.”

In the past, delayed rate cuts have hurt expensive pockets the most — Nasdaq and Indian ITin 2000-01, and Emerging Markets and Indian cyclicals in 2008, pointed out a report by Nuvama Institutional Equities dated 11 September. “Today, Indian midcaps and cyclicals (autos, PSUs, industrials, metals) are such pockets—with decadal-high valuations—we are large UW (underweight) thereof. We maintain a defensive bias (OW – overweight- consumer, telecoms, pharma, insurance).”

The brokerage noted that private banks sector is its sole key cyclical overweight due to its significant underperformance, cheap valuations in a very expensive market, and a narrowing earnings gap with the broader market.

Chaming news for all us

Excellent news for all us