Is Bajaj Housing Finance IPO a gateway to India’s growing housing market?

Source: Live Mint

To understand BHFL’s market positioning and assess its prospects, we present a SWOT analysis.

Standing out in the mortgage market

Bajaj Housing Finance distinguishes itself from competitors with a diversified mortgage lending product suite. Unlike many peers who predominantly focus on home loans, BHFL offers a broader range of products, including home loan (57.8% share in FY24), loan against property (10.5%), lease rental discounting (19.3%), developer finance (10.5%), and others (1.9%). This diversified portfolio enables the company to cater to a wider array of customer needs and mitigates risk by spreading exposure across different product segments. In comparison, competitors like LIC Housing Finance, PNB Housing Finance, Can Fin Homes, Aadhar Housing Finance, Aavas Financiers, Home First Finance, and Aptus Value Housing Finance have a higher concentration in home loans, ranging from 69% to 86%.

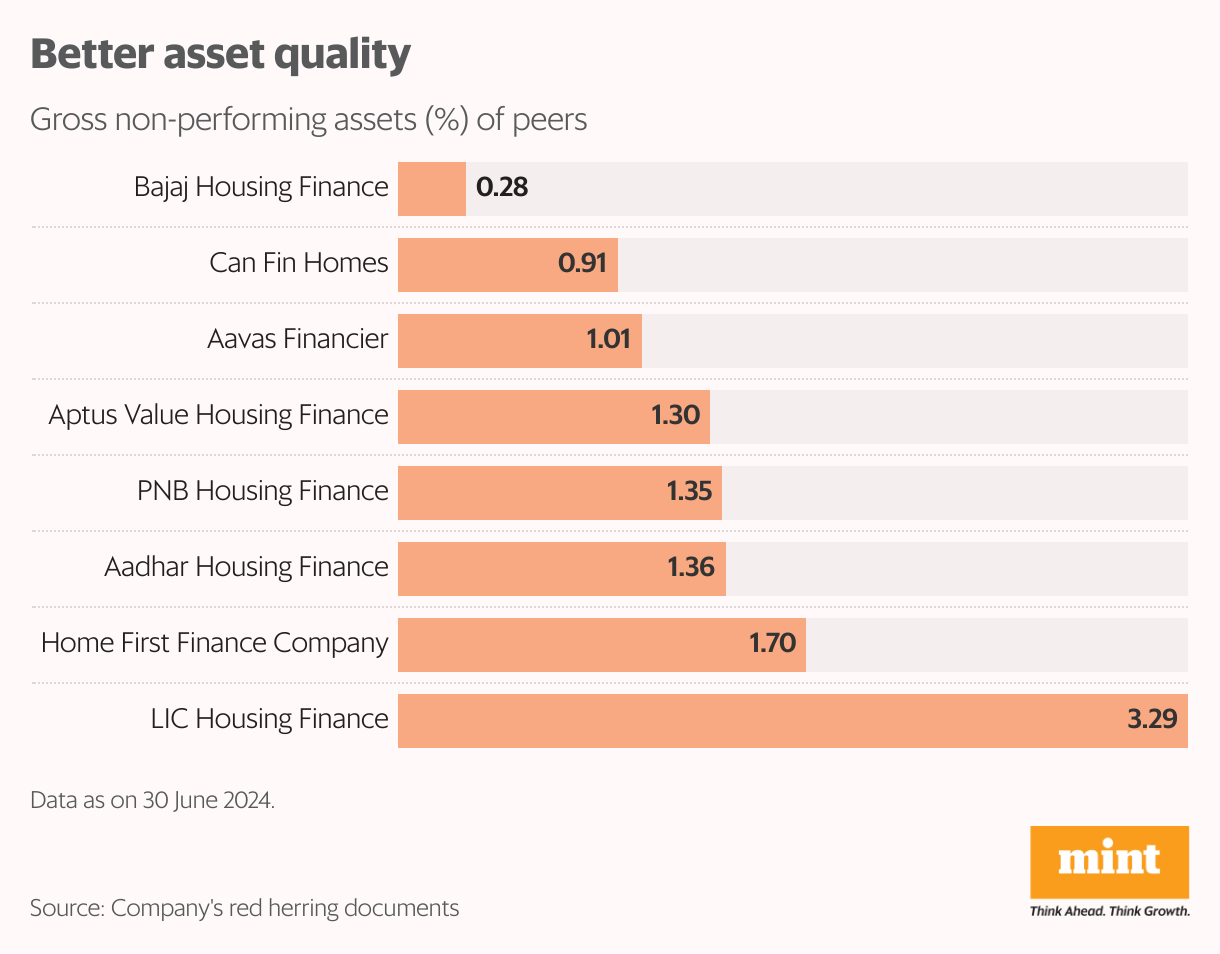

In terms of asset quality, BHFL has excelled with a low gross non-performing assets (GNPA) ratio of 0.28% as of June 2024, demonstrating effective risk management strategies. This ratio is significantly lower than those of its peers, such as LIC Housing Finance (3.29%) and other peer companies with GNPAs ranging from 0.91% to 1.70%.

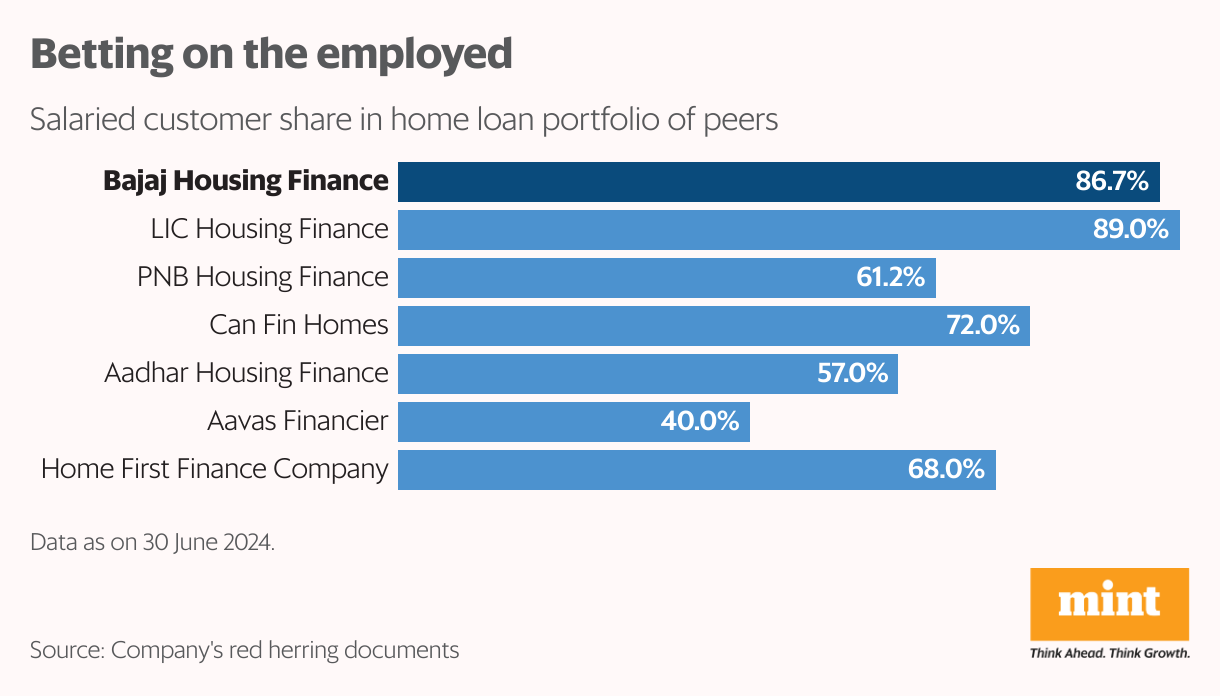

Moreover, it has a strong focus on salaried individuals, known for their financial stability and lower risk profile, with 86.7% of its home loan portfolio consisting of loans to salaried individuals as of June 30, 2024. “Fastestturnaround time due to enhanced digital adoption in loan processing, as well as a high level of digitization incorporated to enhance simplicity and efficiency in customer servicing are the key features of BHFL to attract low-risk salaried customers for their home loan products,” said Jignesh Shial, director of research and head of BFSI sector at InCred Capital.

Also read Baazar Style IPO: Is it a fashionable investment opportunity?

This focus aligns with the company’s strategy of targeting specific customer segments and offering tailored products to meet their needs. “The company plans to maintain its market share across all customer segments, including salaried customers, by adopting a tailored approach based on the unique risks and returns associated with each segment. This strategy serves as a bonding tool, enabling the company to build strong relationships with its customers,” Atul Jain, managing director, Bajaj Housing Finance, told Mint at the IPO launch.

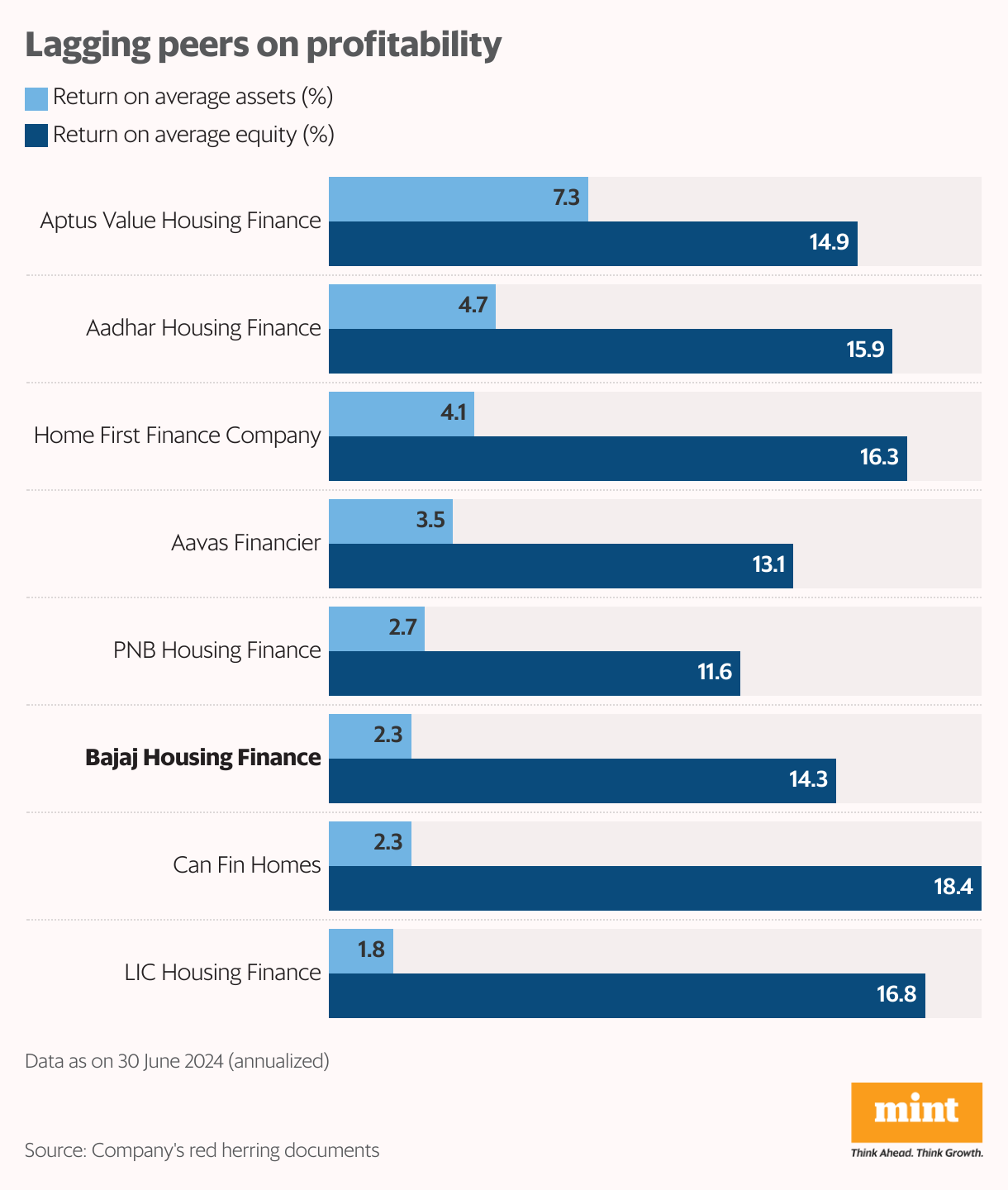

But profitability lags behind competitors

Despite its strengths, Bajaj Housing Finance faces challenges in maintaining profitability compared to its peers. The company’s return on average equity stood at 14.3%, which is notably lower than that of several competitors, including LIC Housing Finance (16.8%), Can Fin Homes (18.4%), Home First Finance (16.3%) and Aadhar Housing Finance (15.9%). “Though the net interest margin profile is relatively vulnerable, there is enough headroom to improve operating efficiency which may drive return on equity outperformance,” said Shial.

Additionally, its return on average assets was at 2.3%, indicating that the company has struggled to generate profits from its assets as efficiently as its competitors including Aptus Value Housing Finance (7.3%), Aadhar Housing Finance (4.7%), Home First Finance Company (4.1%) and Aavas Financier (3.5%) as on June 30, 2024 on annualized basis.

Also read: Ola Electric’s IPO: charging ahead or running on empty?

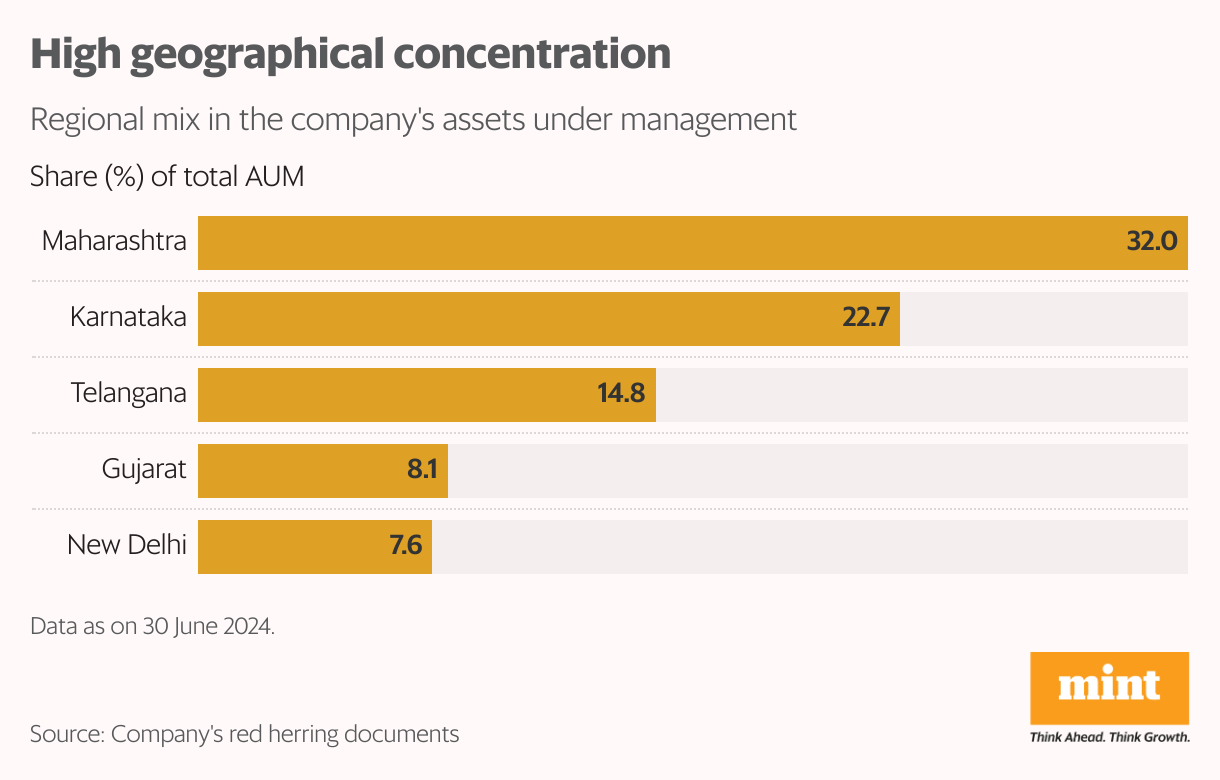

A high geographical concentration is another concern. The company’s assets under management (AUM) are concentrated in a few key states, with Maharashtra accounting for 32.0%, Karnataka 22.7%, and Telangana 14.8% of its AUM as of June 30, 2024. While this concentration gives the company a strong market presence in these regions, it also exposes it to risks if the real estate market or economic conditions in these states deteriorate.

According to Arun Kejriwal, founder of Kejriwal Research and Investment Services, India’s housing finance sector is characterized by a specialized approach, where experts focus on specific market segments such as upper-end, premium, affordable, mid-range, and developer financing. This targeted strategy is a defining feature of the industry, with companies concentrating their efforts in particular regions and adopting a cluster approach to optimize efficiency. By doing so, they can tap into the unique dynamics of each market segment, rather than being bound by geographical location.

External dependencies

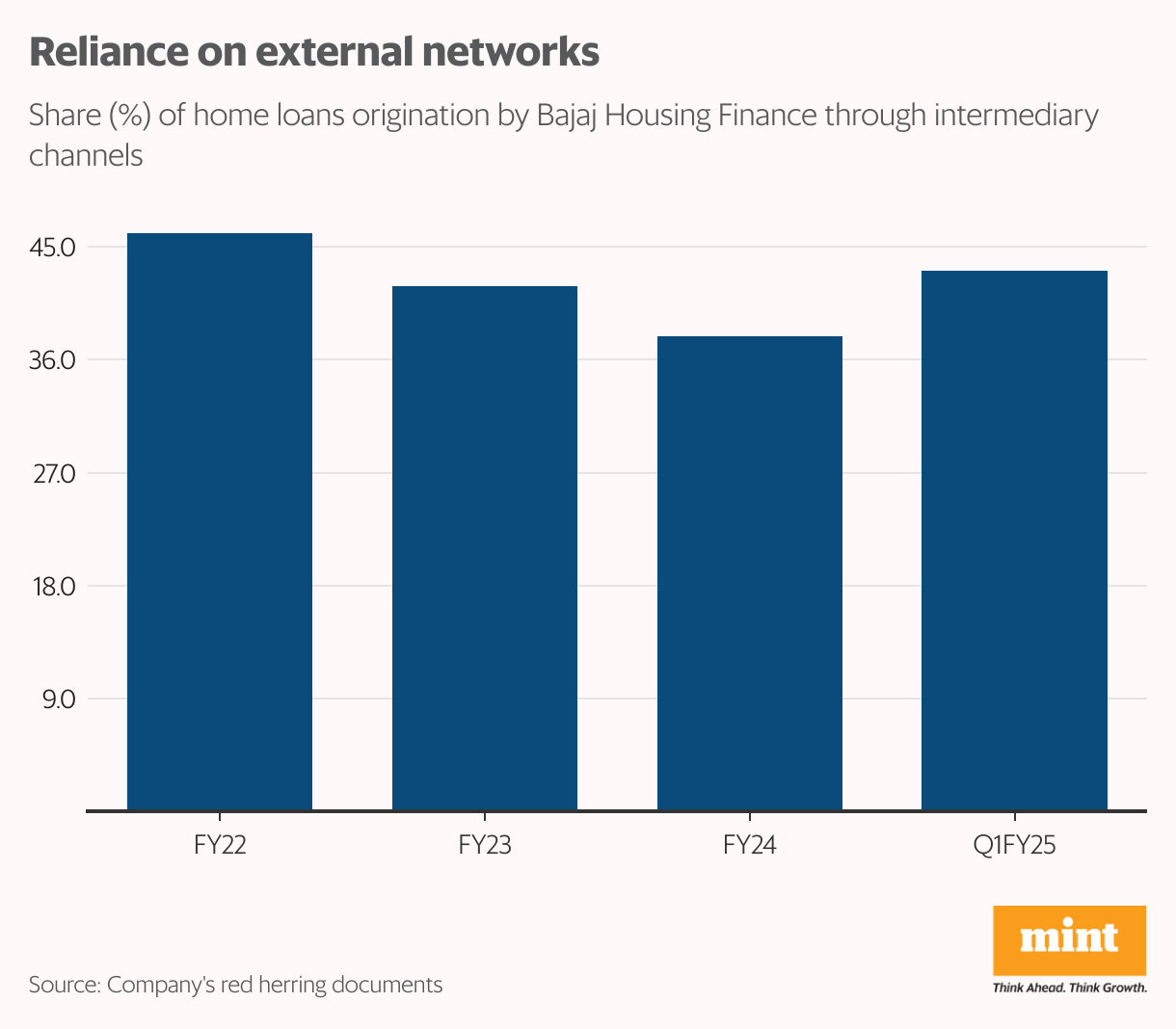

The company’s reliance on external distribution networks for customer referrals—while the share of loans sourced through intermediaries has been declining from 46.1% in March 2022 to 43.1% in June 2024—it exposes the risks associated with losing these channels as they also cater to competitors. Moreover, even as Bajaj Housing Finance has a strong presence in the prime housing finance segment, the segment remains highly competitive with banks dominating in terms of market share in total credit outstanding.

Growth prospects

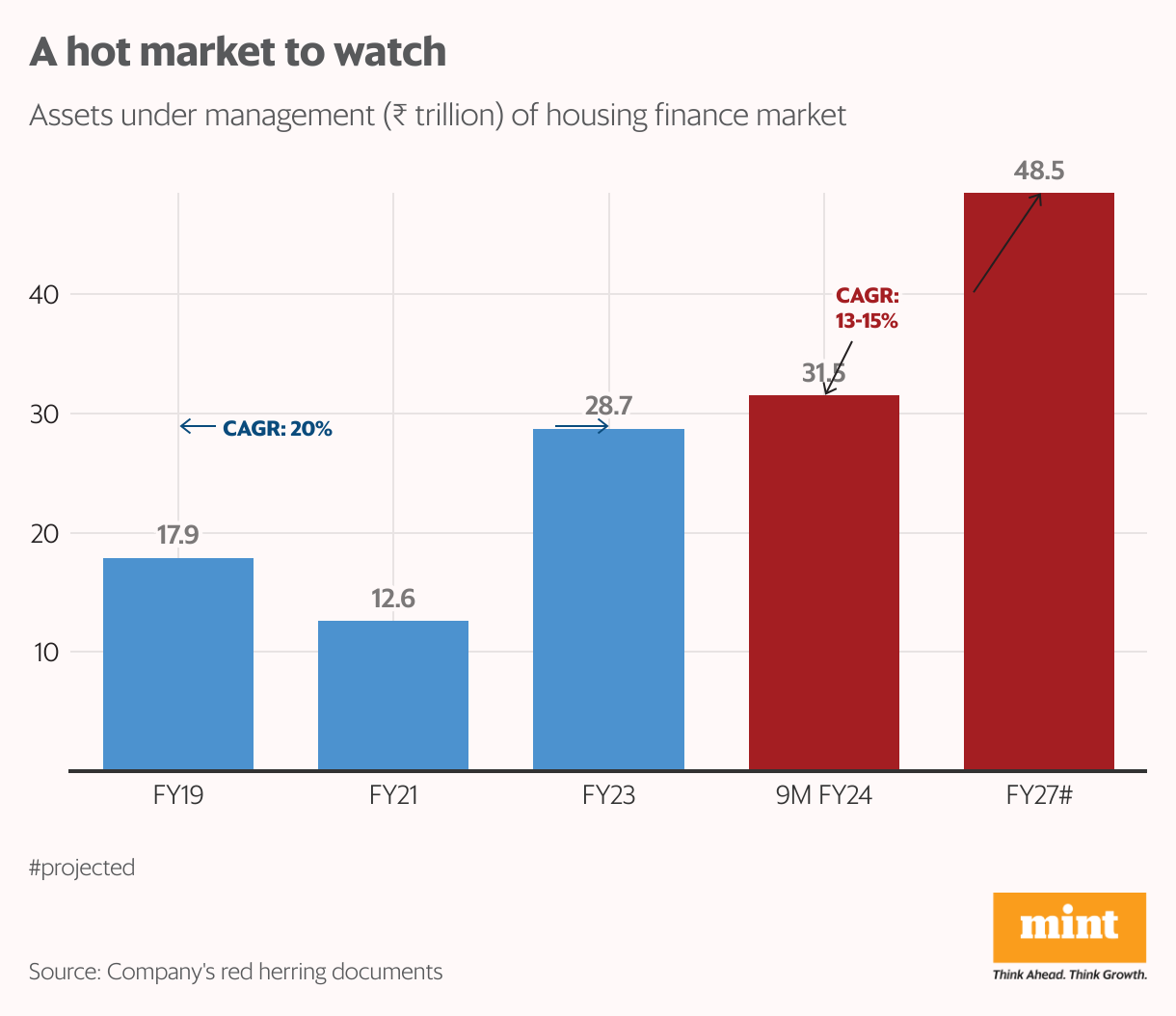

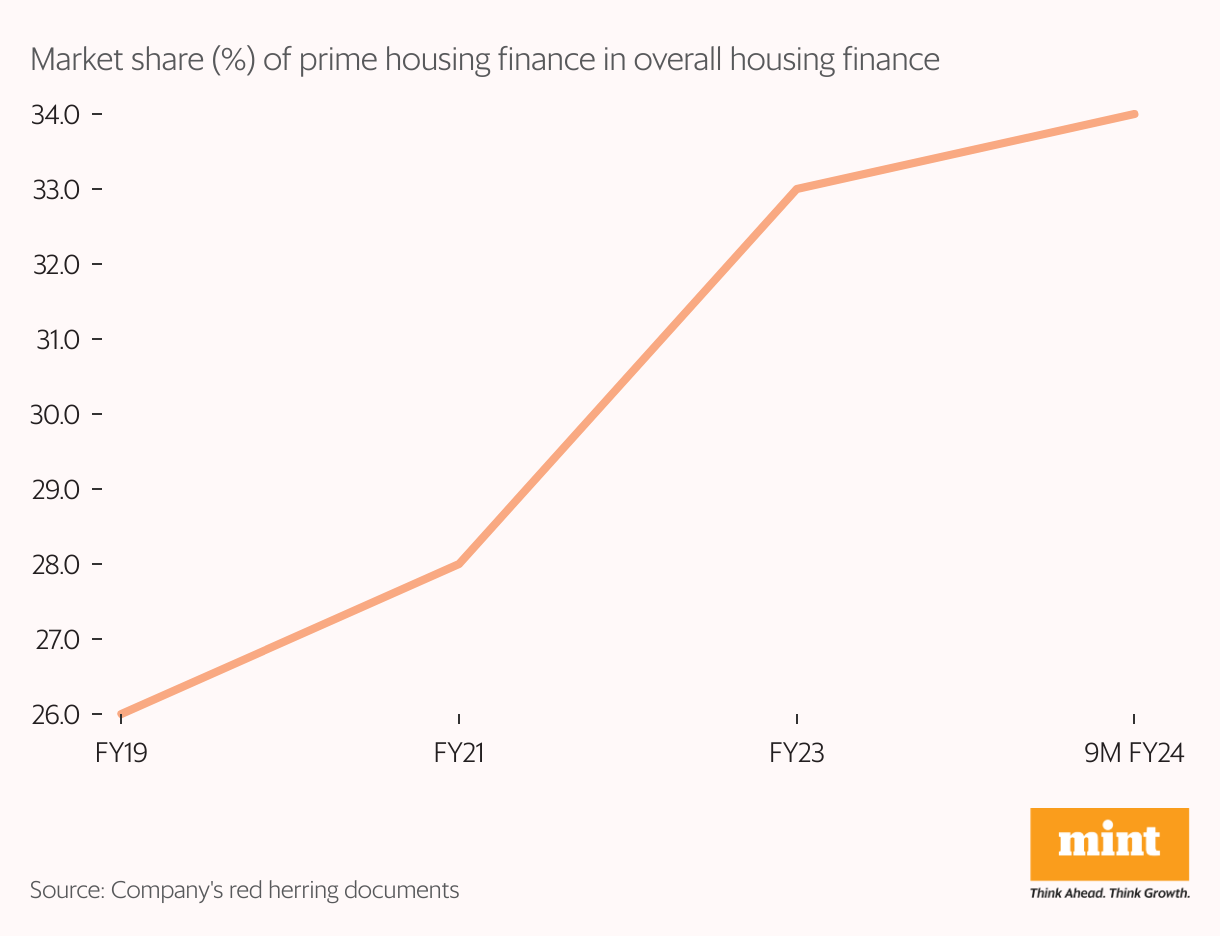

The company focuses on prime housing, the segment that witnessed the fastest growth in housing finance in the last five years is expected to to grow at an annualized rate of 13-15% in the next three years, driven by rising disposable incomes, increasing urbanization, and government initiatives to promote affordable housing. BHFL looks well positioned to capitalize on the expanding housing finance landscape.

Also read: FirstCry IPO: Cracking the baby business code