India Inc’s increasingly important growth driver: The subsidiaries

Source: Live Mint

Subsidiaries have become a significant source of growth for Indian companies, helping them de-risk a bit from their core business.

According to a Mint analysis of 1,135 companies for which the past 15 years of data is available, India Inc now generates 30% of its consolidated revenue through subsidiaries, up from 20% in FY09. importantly, subsidiaries have clocked higher profit growth over this period.

The analysis excludes IT, banking and other financial services companies.

Separating these by sector delivers significantly varying insights. Total consolidated revenue of the sample set stood at more than ₹100 trillion in FY24, with subsidiaries contributing ₹30 trillion. While standalone revenue grew at a 9% compound annual rate over FY09-FY24, subsidiaries’ revenue grew faster at 13%, thus boosting their contribution to the overall pie.

Also read: TCS’ Q2 margin miss drives earnings downgrades

Sectors that saw a sharp spike in contribution from subsidiaries include auto ancillaries (11% to 48%), commodities trading (24% to 54%), pharmaceuticals (22% to 38%) and infrastructure developers & construction (13% to 31%).

While automobile, mining and real estate companies also generated at least 40% of their revenue through subsidiaries, the rise in contribution was less than 10% over this period.

For power generation companies, while the share is still relatively low at 24%, it should increase in the coming years with a large number of green energy projects being undertaken through subsidiaries.

What’s driving the change?

“Indian companies are entering new businesses through subsidiaries for easier technology transfer and/or capital infusion from foreign partners to execute tech- and capital-intensive projects. It also helps derisk parent companies in new-age and high-risk businesses,” said Deepak Jasani, head, retail research, HDFC Securities.

Devising an employee stock options plan (ESOP) and attracting talent for new business is also easier with this structure, Jasani added.

The higher share is also due to large acquisitions that are run as subsidiaries for operational reasons. Among large companies, Reliance Industries Ltd has seen a significant increase in subsidiaries’ share—from 6% to 41%—with its entry into telecom and retail. It’s followed by Larsen & Toubro Ltd (16% to 43%) and Bharti Airtel Ltd (9% to 37%), which have also made acquisitions and expanded into new areas.

Also read: Hitachi is high on energy, but valuation is low on comfort

However, there are some outliers. The steel sector has seen the share drop from 50% to 22% because of Tata Steel Ltd’s acquisition of Corus, which added to the subsidiaries’ share in FY09. The sale of large parts of those assets and higher domestic growth has led to a decline in the share.

Excluding Tata Steel, subsidiaries’ share in the steel sector has increased 7%. Similarly, for non-ferrous metals, subsidiaries’ share has dropped because Hindalco Industries Ltd’s subsidiary Novelis contributed three-fourths of revenue in FY09, which has now fallen because of higher domestic growth.

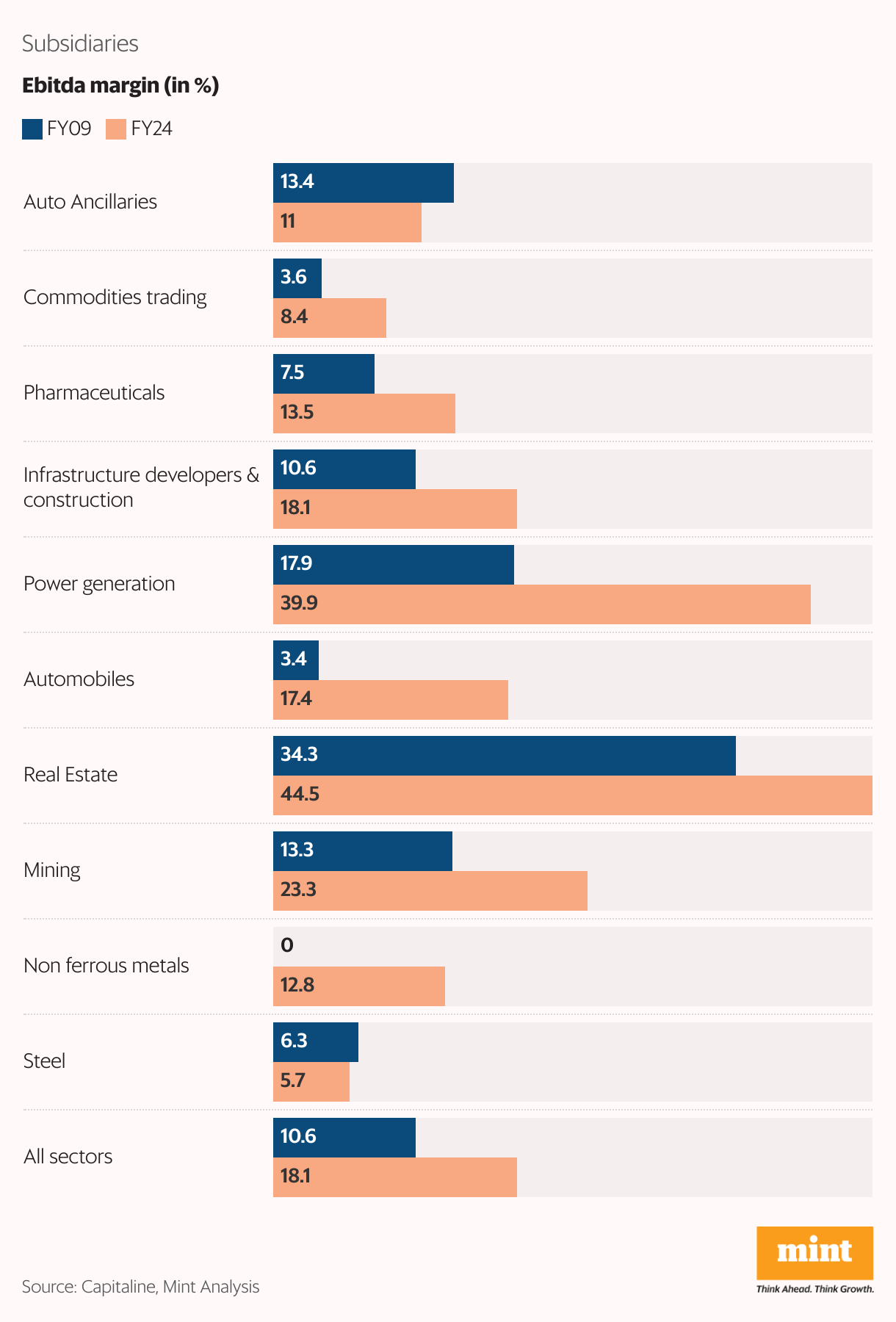

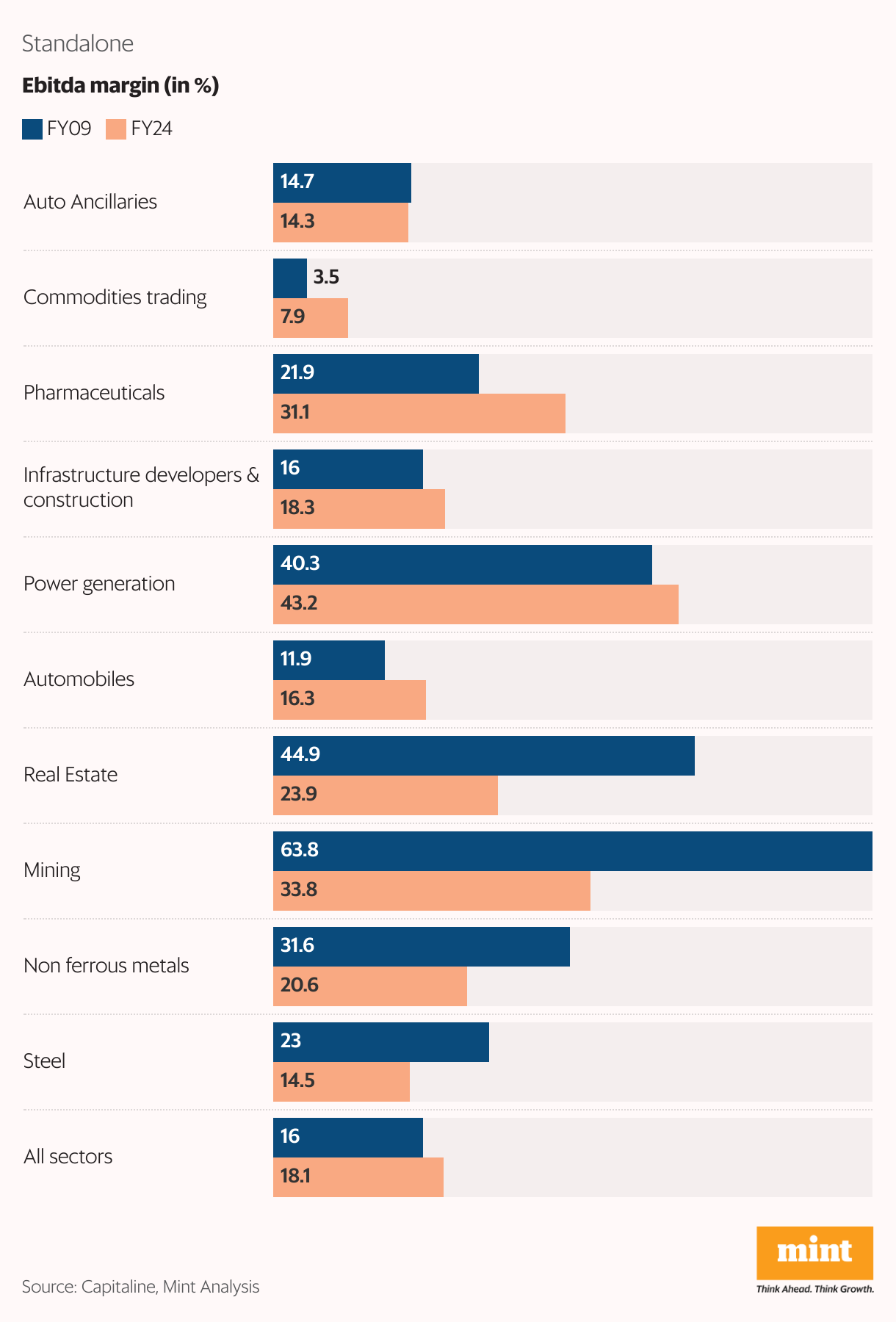

Yet, the bigger aspect of the changing operating structure is the improving profitability of subsidiaries. Against compound annual Ebitda growth of 10% for standalone businesses, subsidiaries have recorded 18% growth over FY09-FY24. Thus, the aggregate Ebitda margin has risen from 11% to 18% while the parent firms’ aggregate margin has improved only slightly, from 16% to 18%.

Also read: Is the recent correction a blip for Indian equities?

Sectors in which subsidiaries have a higher margin than the parent company are real estate, infrastructure development, cement and capital goods.

However, in several sectors such as steel, pharma and agrochemicals, subsidiaries’ margin is significantly lower than that of their parent firms. Thus, an improvement in their profitability, as in other sectors, is something investors are eager to see.