DLF’s ₹1 trillion bet: Can the real estate major stay ahead of a cooling market?

Source: Live Mint

Driving this vision is a potent mix of strong residential monetization, a growing annuity business, and aggressive land acquisitions. DLF plans to double its rental income to ₹10,000 crore by FY30 while boosting dividends to 50% of net profit.

Read this | DLF sees room for growth, but is it too early to be optimistic?

However, with real estate demand showing signs of softening and a heavy reliance on the NCR region, can DLF sustain its winning streak?

Record sales, but a slowdown looms

DLF has thrived on the post-pandemic real estate surge, consistently outperforming its targets.

In 9MFY25, the company posted its highest-ever new sales bookings of ₹19,187 crore, marking a 44% YoY growth—well above its ₹17,000 crore guidance for FY25.

The growth was primarily driven by launches in the luxury and super-luxury segments, with a gross development value (GDV) of ₹40,600 crore. Notably, strong demand for the premium Dahlias project, which contributed ₹11,800 crore in Q3FY25, further propelled sales.

However, this breakneck pace is slowing. DLF has projected flat pre-sales for FY26, citing a slowdown in new launches across Delhi NCR and Mumbai—where it has recently expanded.

That said, the company remains well-positioned for long-term growth, backed by a robust project pipeline worth ₹1.14 trillion from FY25 onward. This includes ₹40,600 crore in projects already launched by Q3FY25 and an additional ₹73,900 crore planned in the coming years.

Moreover, DLF expects to roll out projects with a GDV of ₹20,000 crore in FY26, reinforcing its pipeline for sustained expansion.

Higher prices, bigger margins

Sustained demand and a strong launch pipeline have driven consistent value appreciation across DLF’s premium portfolio, reinforcing its position in the luxury real estate market.

According to Nuvama, property prices in DLF projects have appreciated at an annual rate of 12-14% over the past decade, with super-luxury properties seeing even stronger gains of 17-18%.

This steady price appreciation, coupled with robust sales—new sales bookings grew at a CAGR of 58% from FY21 to 9MFY25—has significantly boosted DLF’s profitability. Embedded margins expanded at a staggering CAGR of 77% to ₹11,500 crore, while net profit surged at a 40% CAGR to ₹1,702 crore in 9MFY25, up from ₹443 crore in FY21.

DLF’s residual gross margins—profits from pre-sold properties yet to be recognized—more than doubled from ₹9,370 crore in FY20 to ₹20,145 crore by Q3FY25. These earnings will be realized gradually as projects progress.

Additionally, DLF holds a substantial level of unsold inventory with a gross margin of ₹17,000 crore. Its upcoming project pipeline is expected to generate ₹30,000 crore in gross margin, bringing the total margin potential to ₹67,000 crore over the medium term.

Read this | DLF’s second going: Can the real estate giant succeed beyond its comfort zone?

Looking ahead, DLF aims to maintain a 45% gross margin while stable new sales bookings are expected to drive a twofold increase in future profits and cash flows.

Strong cash flows enable expansion

DLF has successfully converted its strong sales and margins into robust operating cash flows, which surged ninefold from ₹406 crore in FY21 to ₹3,863 crore in 9MFY25.

Steady cash generation has enabled the company to reinvest in land acquisition—a key priority for sustaining future launches. Land-related capex climbed to ₹1,508 crore in 9MFY25, up from ₹202 crore in FY21, and stood at ₹2,248 crore in FY24.

By securing a steady pipeline of projects, DLF is positioning itself for long-term growth and earnings visibility over the next two decades. A strong pipeline of upcoming launches and unsold inventory further reinforces its ability to generate sustained cash flows.

According to Nuvama, DLF is set to generate ₹10,000 crore in operating cash flow from sales already made (post-construction costs) and ₹24,000 crore from unsold inventory. Planned launches are expected to contribute an additional ₹24,000-26,000 crore.

This would result in a surplus of ₹41,000 crore after accounting for capex, overheads, and taxes. Combined with its ₹9,000 crore cash reserves as of Q3FY25, DLF’s total cash surplus is projected to reach ₹50,000 crore over the medium term.

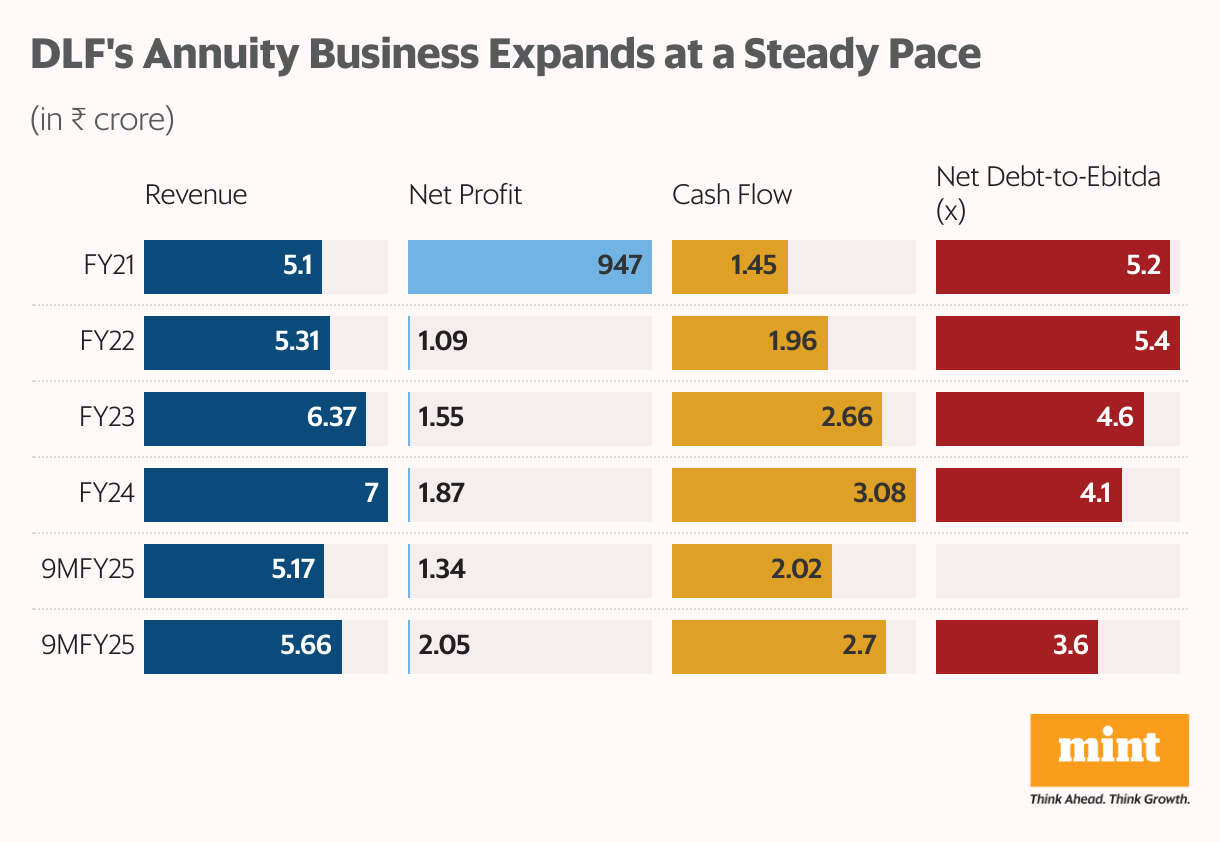

Steady annuity growth

DLF’s annuity business—spanning office, retail, hospitality, and asset management—operates under the Development Company (Devco) and DLF Cyber City Developers (DCCDL) brands.

Read this | Voltas rides the summer wave. But is the stock still a cool bet?

The company currently manages an operational rental portfolio of 39 million square feet (msf) in office spaces, with 36 msf under DCCDL and the rest under Devco. Its retail segment spans 4.3 msf, boasting an impressive 98% occupancy rate.

Looking ahead, DLF plans to expand its annuity portfolio to 73 msf, including 60 msf of office and 13 msf of retail properties. To support this growth, it has committed ₹20,000 crore in incremental capex for developing 29 msf. Even after this expansion, the company retains 62 msf of development potential, ensuring sustained long-term growth.

While DLF’s annuity business grows at a steadier pace than its real estate segment, it provides diversification and a stable income stream. Annuity income has risen at an 8% CAGR, from ₹5,102 crore in FY21 to ₹6,996 crore in FY24, reaching ₹5,655 crore in 9MFY25.

DLF’s annuity revenue includes ₹4,633 crore from rental income, which it expects to double from ₹5,000 crore in FY25E to ₹10,000 crore by FY30E. Meanwhile, net profit has grown at a 21% CAGR over the past four years, reaching ₹1,866 crore in FY24 and ₹2,053 crore in 9MFY25.

This strong profitability has fuelled robust cash flows, which grew at an 18% CAGR to ₹3,080 crore in FY24 and ₹2,704 crore in 9MFY25. With sustained operating cash flows, DLF’s annuity business has also reduced leverage, bringing its net debt-to-Ebitda ratio down from 5.2 in FY21 to 3.6 in Q3FY25.

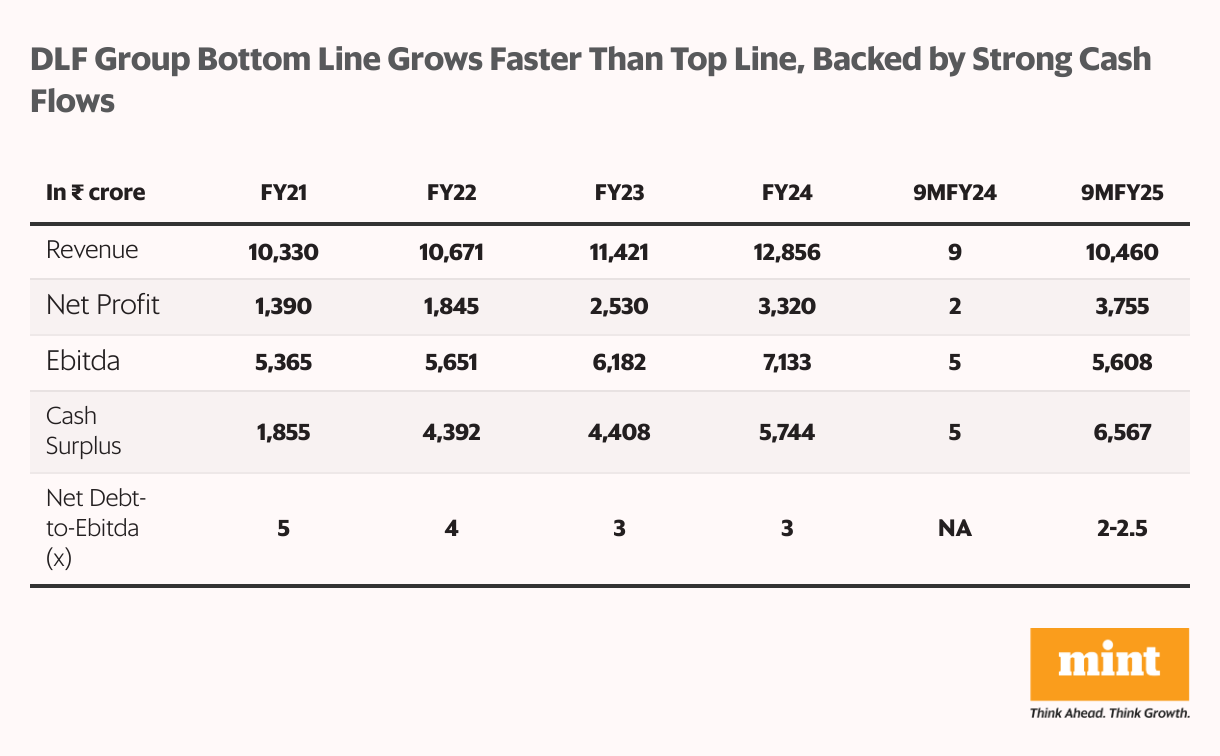

Strengthening the balance sheet

DLF’s strong performance across its residential and annuity businesses has led to steady growth in revenue, Ebitda, and profitability over the past four years.

Despite a modest 5.6% CAGR in revenue, which reached ₹12,856 crore in FY24, group profit surged at a robust 24% CAGR to ₹3,320 crore from ₹1,390 crore in FY21. Meanwhile, Ebitda grew at a steady 7.4% CAGR to ₹7,133 crore over the same period.

This financial momentum has translated into a growing cash surplus, which tripled from ₹1,855 crore in FY21 to ₹5,744 crore in FY24 and further increased to ₹6,567 crore in 9MFY25. As of 9MFY25, DLF holds a net cash surplus of ₹4,534 crore, marking a sharp turnaround from its net debt of ₹4,885 crore in FY21.

Beyond reinvesting in land, DLF has strategically used its surplus cash to reduce group-level debt, which declined from ₹24,028 crore in FY21 to ₹14,679 crore in 9MFY25. Gross debt also fell to ₹4,435 crore, down from ₹6,511 crore in FY21. This has improved its net debt-to-Ebitda ratio, from 4.5x in FY21 to an estimated 2-2.5x in FY25, reinforcing its balance sheet strength.

Building on this momentum, the company aims to achieve net debt-zero status at the group level by FY30, supported by rising operating cash flows.

Read this | UltraTech cements its lead—and looks to build on it

Alongside debt reduction, DLF has maintained a strong dividend track record, paying dividends for 17 consecutive years. Between FY21 and FY24, it increased its payout 2.5 times to ₹1,238 crore in FY24, driven by higher profitability. Looking ahead, DLF plans to move toward a payout ratio of 50% of net profit, reinforcing its commitment to shareholder returns.

Key risks

Despite its strong fundamentals, DLF faces key risks.

Its heavy reliance on the NCR region, where 60% of its land bank is concentrated, poses a geographic concentration risk. Additionally, the long gestation period for monetizing its land bank—often exceeding two decades—limits flexibility.

DLF also has a relatively limited presence in the affordable and mid-income housing segments, where demand is more resilient.

Further, a slowdown in price appreciation due to declining real estate affordability and softer demand remains a concern.

Elevated valuation

DLF trades at an EV/Ebitda multiple of 60, a 30% premium to its five-year median multiple of 46.

Relative to peers, it commands a 90% premium over Macrotech and a 60% premium over Godrej Properties. While this premium reflects its market dominance, annuity revenue, and improved fundamentals, valuations remain elevated.

For more such analyses, read Profit Pulse.

Kotak Securities suggests the current price already factors in a potential demand slowdown and has set a target of ₹1,020.

About the Author: Madhvendra has been a passionate follower of the equity market for over seven years and a seasoned financial content writer. He loves reading and sharing his opinions about publicly listed Indian companies and macroeconomic trends.

Disclosure: The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.