Can Hyundai’s IPO succeed in a slow auto market?

Source: Live Mint

While the passenger vehicle market is currently facing headwinds, is Hyundai’s IPO a strategic gamble? With the beginning of the festivities, could the timing signal the beginning of a new growth chapter for the company, capitalizing on increased consumer sentiment and potential market rebound?

As HMI prepares to gauge investor sentiment, a comprehensive SWOT analysis will offer crucial insights into its post-IPO trajectory and potential to redefine India’s automotive landscape.

A strong engine

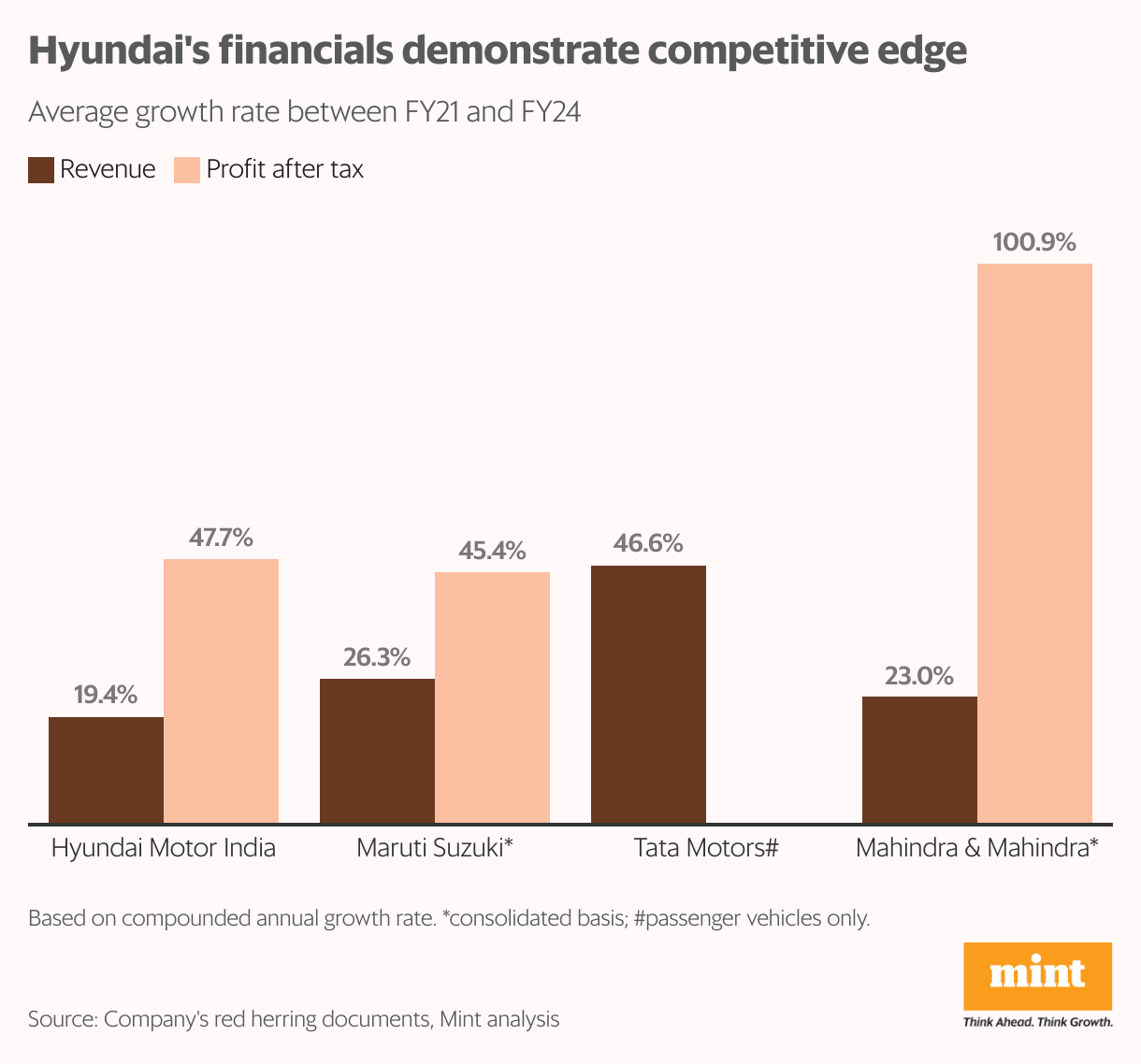

The company has demonstrated strong financial performance over the past few years. Its topline has grown steadily and witnessed a compound annual growth rate of nearly 20% over the past four years, while its bottomline expanded at an even faster pace, 48% during this period. The company’s profitability has been supported by strong operational efficiency: return on capital employed and operating margins have recorded a three-year median of 29% and 13%. Tarun Garg, chief operating officer of Hyundai Motor India further boasted of its market position at a recent press meeting: “We have consistently maintained our position as the second-largest OEM in the market, not just in volume but also with a solid market share.” Adding to the prospects, he said that the upcoming new plant in Pune, will increase the production capacity from 824,000 to nearly 1.1 million units. This strategic move will enable HMI to cater to the growing demand while solidifying its leadership position.

Hyundai’s efficient sales and service network, with a remarkable 1.1 sales-to-service outlet ratio, sets it apart from competitors like Tata Motors and Maruti Suzuki, ensuring unparalleled customer satisfaction.

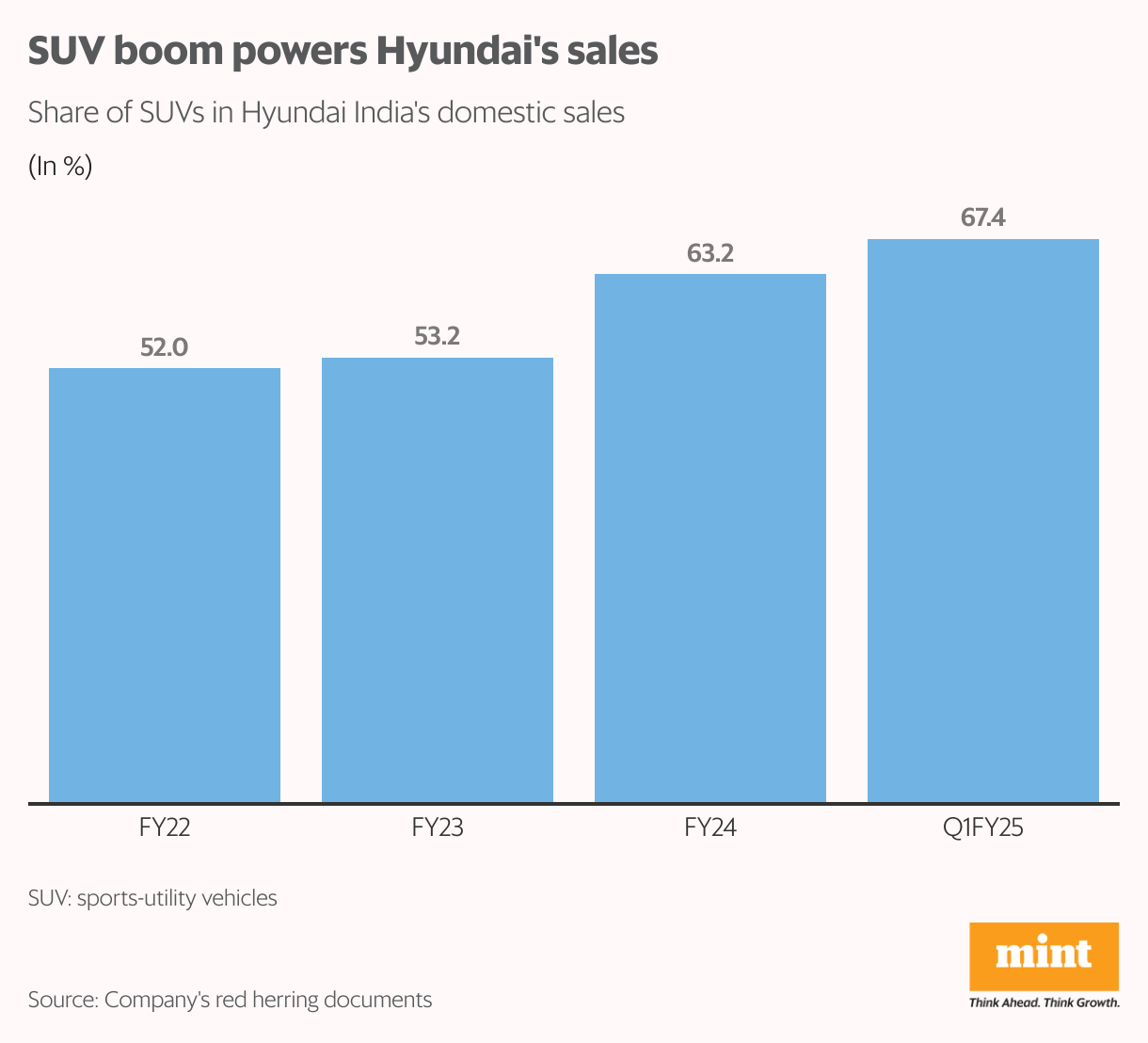

Further, HMI’s strategic alignment with the rising popularity of SUVs in India has fueled its impressive growth: between FY22 and FY24, the domestic sales volume of its SUVs has witnessed a steady increase, rising from 52.1% of its domestic sales to 63.2%. This growth underscores the company’s ability to cater to the evolving preferences of Indian consumers.

Also read Missed the Bajaj Housing IPO boat? There’s still time to get on deck.

Its diverse portfolio of 13 passenger vehicle models, including the Aura, Verna, Grand i10 NIOS, i20, i20 N Line, Exter, Venue, Venue N Line, Creta, Creta N Line, Alcazar, Tucson, and IONIQ 5, has catered to various customer preferences. Moreover, its strategy of frequently launching facelifts for its models has kept it ahead of its peers in this approach. “This approach has become a common strategy among various companies, but its effectiveness depends on the specific demand for each brand or model in the market,” explains Abhishek Gaoshinde, deputy vice president of research at Sharekhan by BNP Paribas. By refreshing their offerings regularly, Hyundai encourages consumer engagement and dealership visits, further solidifying its competitive edge.

Time to adapt

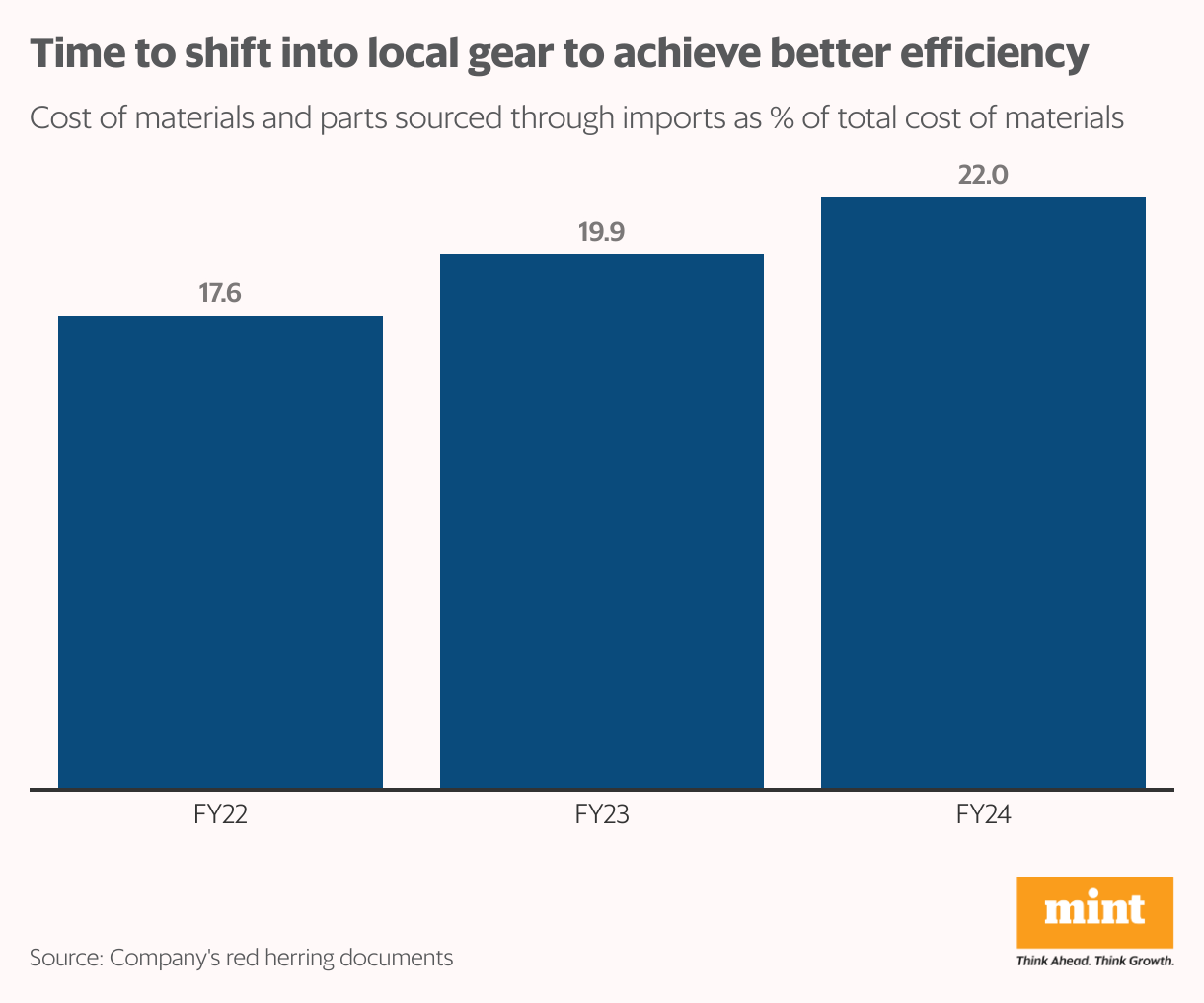

Meanwhile, with imported materials and parts accounting for nearly 22% of Hyundai’s cost of goods sold, up from 18% in FY22, the company faces a pressing need to shift into local production to improve efficiency and reduce costs.

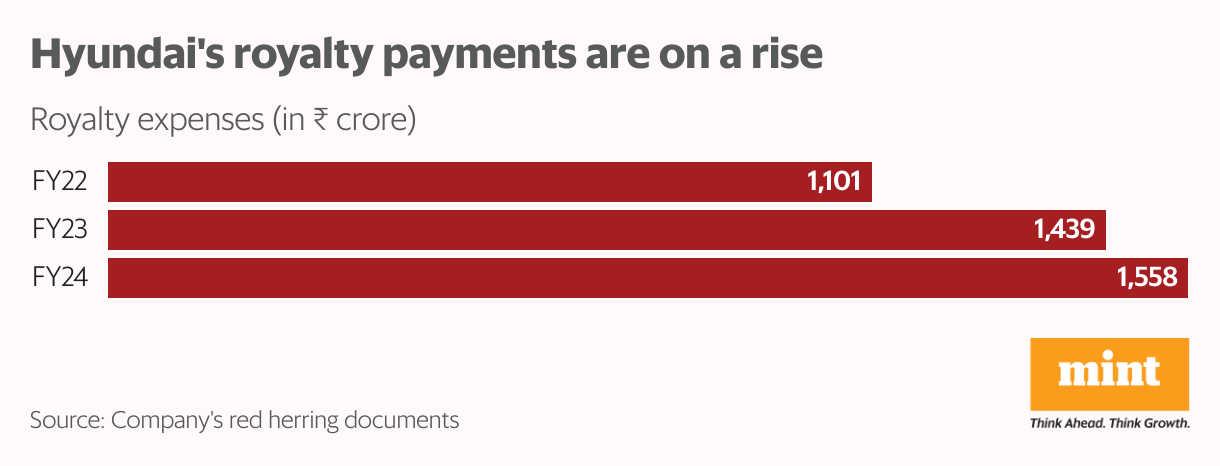

Additionally, the company’s royalty expenses have risen from ₹1,101 crore in FY22 to ₹1,558 crore in FY24, recording a substantial growth of 41.6%. However, it has remained stable as a share of revenue fluctuating between 2.23% and 2.75%. “Under the previous royalty agreement, payments were tied to specific vehicle models sold. However, with the new agreement, royalty is now set at a fixed 3.5% of annual sales,” explained Sreeram Ramdas, vice president at Green Portfolio. “This 3.5% aligns with agreements the parent company has with other global subsidiaries. However, Hyundai India currently enjoys a high EBIT margin of 10.1%, which is unlikely to hold once the new royalty terms take full effect.”

Also read IPO invincibles: Beyond KRN, more IPOs that defied the market crash

Adding to the concerns, Saji John, senior research analyst at Geojit Financial Services said that royalty payments are currently at a historic high of 3.5% of sales revenue and could rise to 5% without requiring minority shareholder approval. This increase could strain profitability, especially if input costs rise or investments in future mobility increase.

Moreover, Hyundai’s limited presence in the electric vehicle (EV) segment presents a strategic challenge, especially as the government accelerates efforts toward sustainable mobility. However, Kranthi Bathini, director of Equity Strategy at WealthMills Securities, believes this is not an immediate concern. “Hyundai is focused on the higher end of the EV market and has the technology to expand as the market develops. They are slowly entering the EV space,” he explains.

Others also don’t see any clouds gathering over its horizon due its limited presence. “Instead of aggressively rolling out EV models, the company is cautiously observing market trends,” notes Ramdas.

The company has maintained profitability and market share with its non-EV models, launching nine upgrades and changes between January 2023 and March 2024. This strategy, particularly in the SUV segment, has driven growth, John said “Given Hyundai’s strong position in the global EV market, we don’t anticipate any immediate pressure, as the company is set to launch multiple EVs soon and aims to ramp up production, aligning with the domestic EV ecosystem while sustaining current capacity utilization.”

Also read The IPO roulette has more spinners and fewer winners, what’s your fate?

Navigating competitive landscape

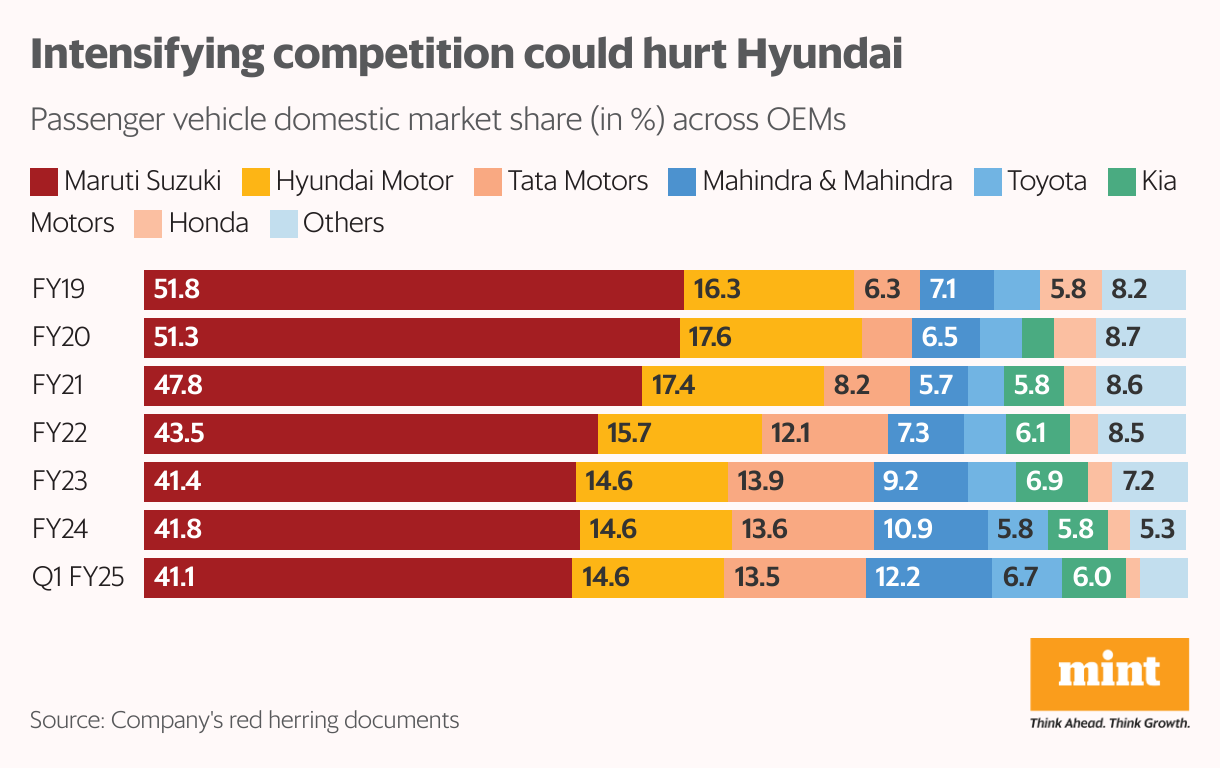

HMI, though backed by the might of the Hyundai Motor Group, finds itself caught in a competitive crossfire. Rivals and its sister brand, Kia, are breathing down its neck: its market share in the passenger vehicles segment has declined from 17.6% to 14.6% in the last five years. Over these years, the competition has intensified amidst competitively priced feature-rich vehicle launches by all players as well as recent entrants such as Kia and MG grabbing sizable shares.

Sister brand Kia has been gaining market share at a faster pace than Hyundai, further complicating the competitive landscape. Though assuaging these concerns, Gaoshinde explains that they operate in the same market but are positioned differently. “Both companies are profitable, yet Kia Corp is gaining more market share than some other competitors. “While they belong to the same group, their business strategies are independent, with each having its own leadership, marketing styles, and segmentation approaches,” he added.

On this, Bathini further added “This brand and product diversification within the group means Kia’s market share growth isn’t a major concern for Hyundai. Both companies are competitive but operate independently, and this structure helps them target different segments without significantly impacting each other’s market share.”

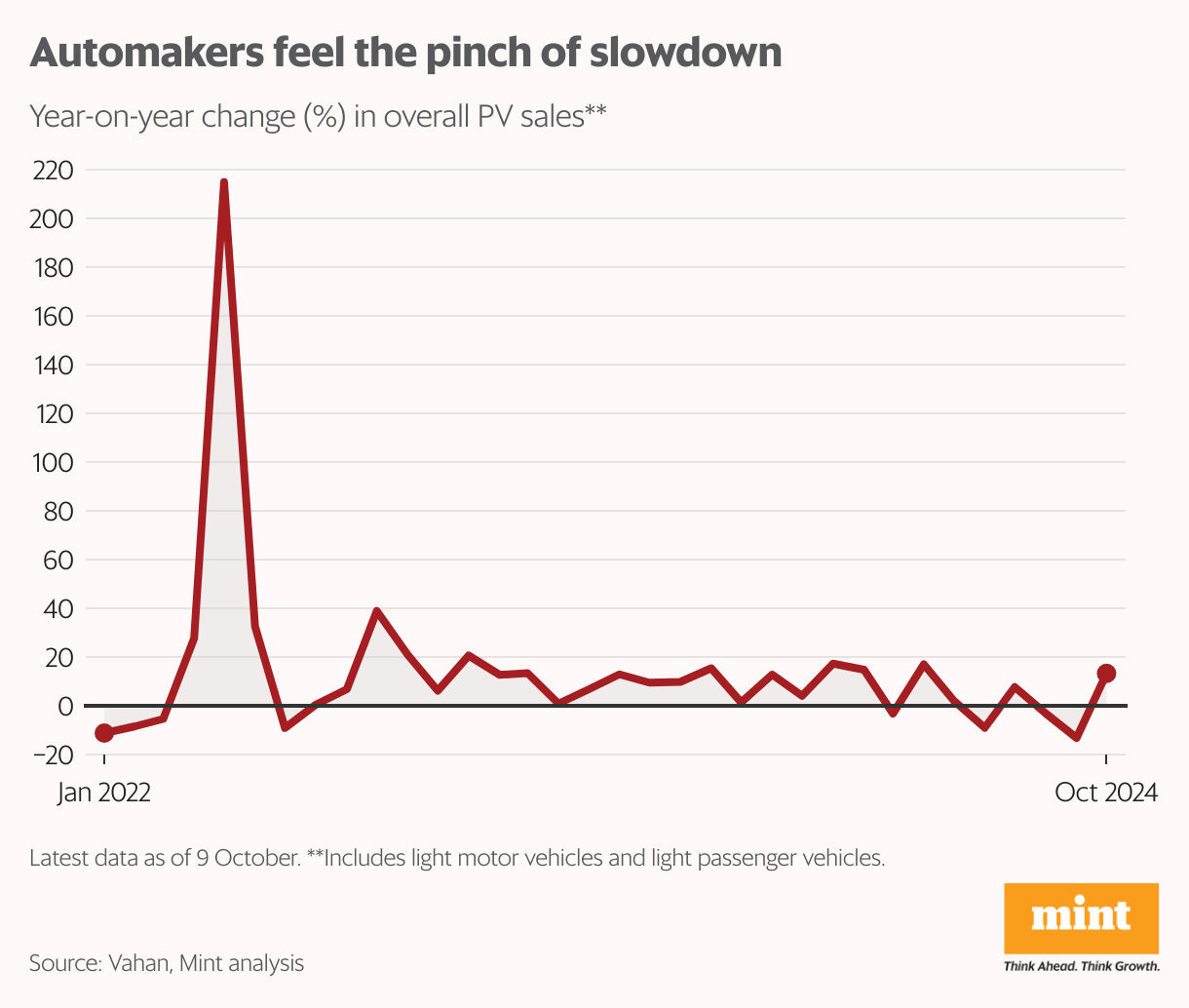

To add to the pressure, the broader automotive market is experiencing a slowdown, making Hyundai’s journey even more challenging. The passenger vehicles sales is on a slow lane with sales either contracting or remaining muted over the past few months on a year-on-year basis. All hopes are pinned on the festivals to revive consumer sentiments.

Riding the SUV wave

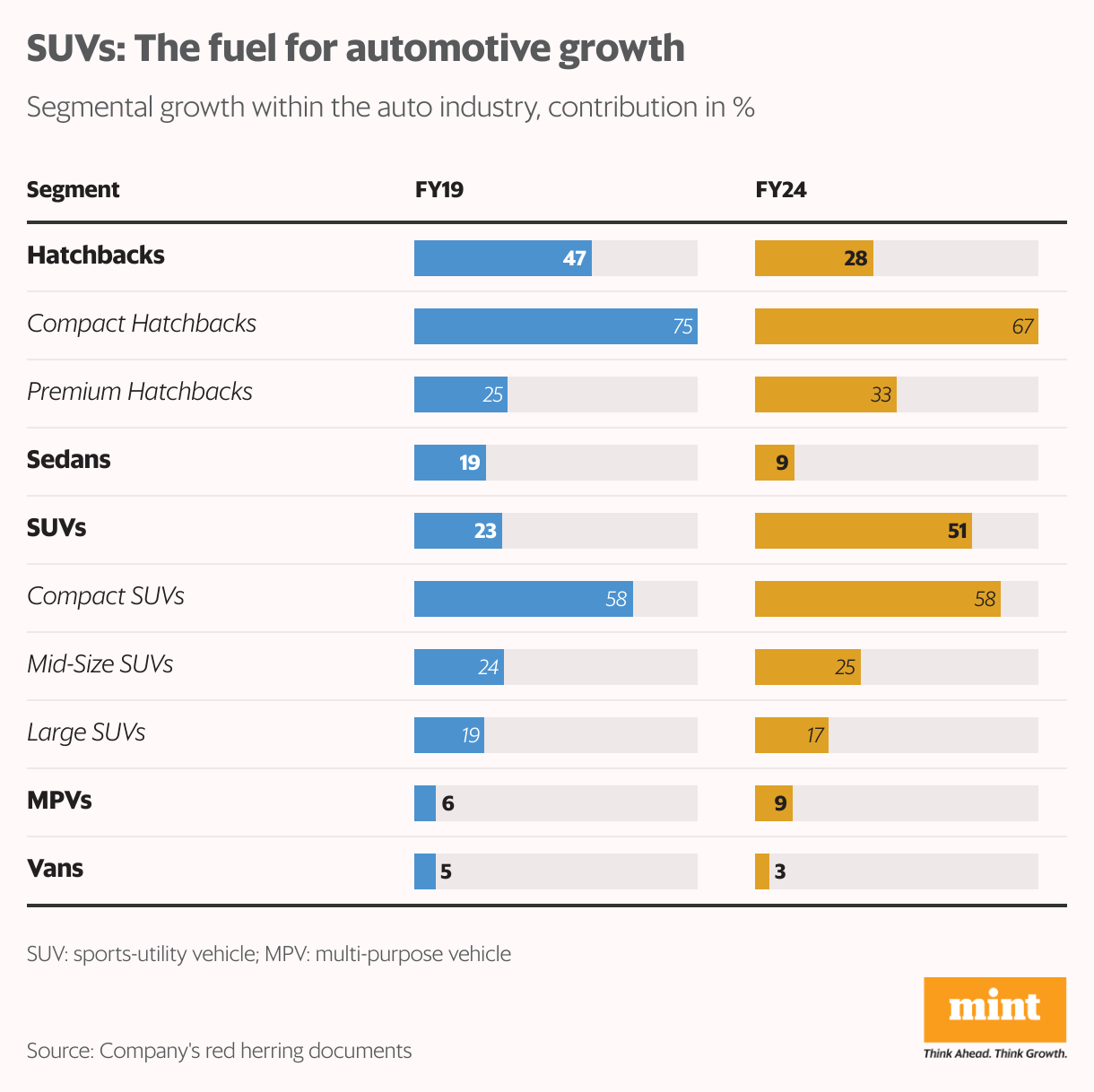

The passenger vehicles market has witnessed a major shift in customer preference: The sports-utility vehicles (SUVs) segment has emerged as the dominant force in the automotive industry.The post-pandemic surge in spending among the upper middle class, coupled with the proliferation of SUV models and increased affordability of compact SUVs, has led to a shift away from hatchbacks and compact sedans, driving up SUV sales and bolstering profit margins. All sub-segments within the SUV category have shown growth rates, significantly outpacing the hatchback and sedan segments. Further, the Passenger vehicle segment in India is expected to grow at a compounded annual growth rate of 7% to 9% in the next five years, according to the CRISIL Report.

Hyundai, which successfully maintained its position as the leading auto OEM in India by sales volume within the mid-size SUV segment since FY19, looks well positioned to capitalize on this opportunity by leveraging its strong brand presence, extensive dealer network, and innovative product offerings. Creta, in particular, achieved an impressive market share of 38% in this sub-segment. Additionally, in FY2024, the Verna emerged as the top-selling model in the premium sedan segment, while the Aura secured its place as the second-highest-selling sedan, capturing a notable 15% market share during the same period.

Furthermore, Hyundai’s entry into the electric vehicle market with the launch of its first premium EV, the IONIQ 5 in 2023 marks a significant step in aligning with global trends towards sustainable mobility. As consumer preferences shift, Hyundai’s proactive approach to expanding its EV portfolio positions the company favorably in the evolving automotive landscape.