UltraTech cements its lead—and looks to build on it

Source: Live Mint

The momentum is fuelled by a recovery in infrastructure spending, industry consolidation, and rising prices—all of which favour dominant players. With government-led capex driving demand and competition weeding out smaller players, UltraTech is poised to gain further ground.

Read this | Is the cement sector consolidation at its fag end?

But challenges remain, from pricing pressures to its bold venture into the cables and wires (C&W) business.

Cement demand recovery gains traction

Infrastructure spending took a hit in the first half of FY25, as elections and monsoons slowed project execution, dampening cement demand. The resulting low volume growth and soft pricing intensified competition across the sector.

However, with government capex rebounding in Q3 and activity picking up post-monsoon and festive season, demand has strengthened. Cement prices have followed, rising ₹5 per bag in February.

Despite recent fiscal tightening, the government remains committed to infrastructure-led growth. Over the next five years, ₹4.6 trillion has been allocated across key projects, including the National Infrastructure Pipeline (NIP), PM Awas Yojana, and highway development.

This sustained investment underpins the sector’s long-term growth potential, with cement volumes projected to rise 7-8% annually through FY27, while revenues are expected to grow at an even faster clip, driven by improved realizations.

Industry consolidation strengthens market leaders

A prolonged price war, fuelled by aggressive capacity expansion amid weak demand, has squeezed margins across the cement sector. Realizations declined 7% year-on-year in FY25 (until January), with smaller players hit the hardest—many facing cash constraints and ultimately becoming acquisition targets.

This wave of consolidation has reshaped the industry. Notable deals include Adani Group’s acquisition of Ambuja Cements and ACC, Dalmia Bharat’s purchase of Jaiprakash Associates, Ambuja’s takeover of Sanghi Industries, and UltraTech’s acquisition of India Cements.

According to rating agency Crisil Ltd, an estimated 11% of India’s installed cement capacity has changed hands in the past two years—the fastest pace of consolidation the sector has ever witnessed.

Larger players such as UltraTech, ACC, Ambuja, and Dalmia Bharat hold a clear advantage, leveraging their financial muscle to scale up rapidly. While organic expansion enhances economies of scale, inorganic growth strengthens market positioning by improving geographical reach, access to raw materials, and cost efficiencies across logistics and operations.

A UBS report projects that by FY30, the top two players will control 44% of the market—solidifying their dominance in an increasingly consolidated landscape.

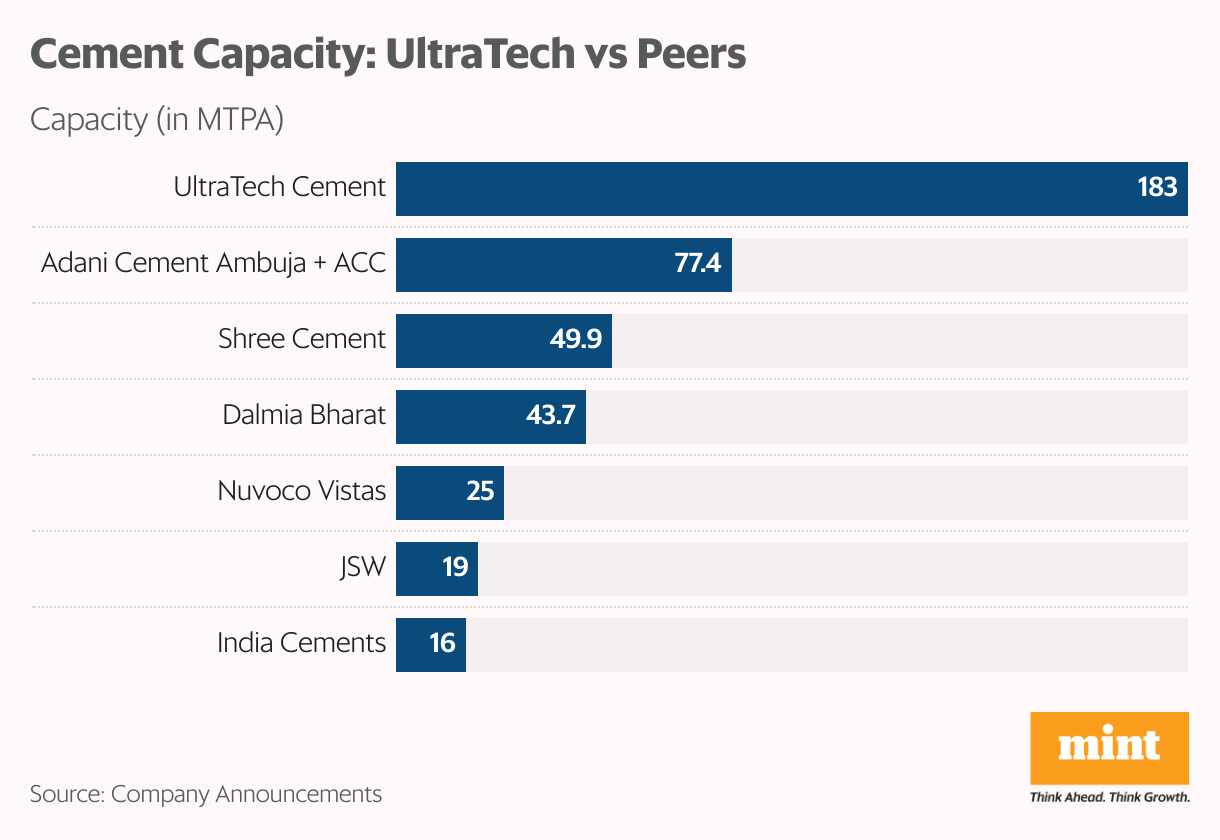

UltraTech: Cementing market dominance

As the undisputed market leader, UltraTech Cement is best positioned to capitalize on the sector’s growth. Backed by the Aditya Birla Group, the company has built an extensive distribution network since its founding in 2000. With a production capacity exceeding 180 million tonnes per annum (MTPA), it commands a dominant 28% market share.

UltraTech’s expansion strategy remains aggressive. In the quarter ended December 2024, it operated at 73% capacity utilization and added 1.8 MTPA in new capacity. With ongoing organic and inorganic investments, it aims to reach 209 MTPA by FY27—further solidifying its lead.

The company’s domestic sales volumes grew nearly 10% sequentially in the December quarter and are projected to expand at an 11% CAGR between FY24 and FY27. As realizations improve, revenue growth is expected to outpace volume expansion, reinforcing UltraTech’s position at the forefront of the industry.

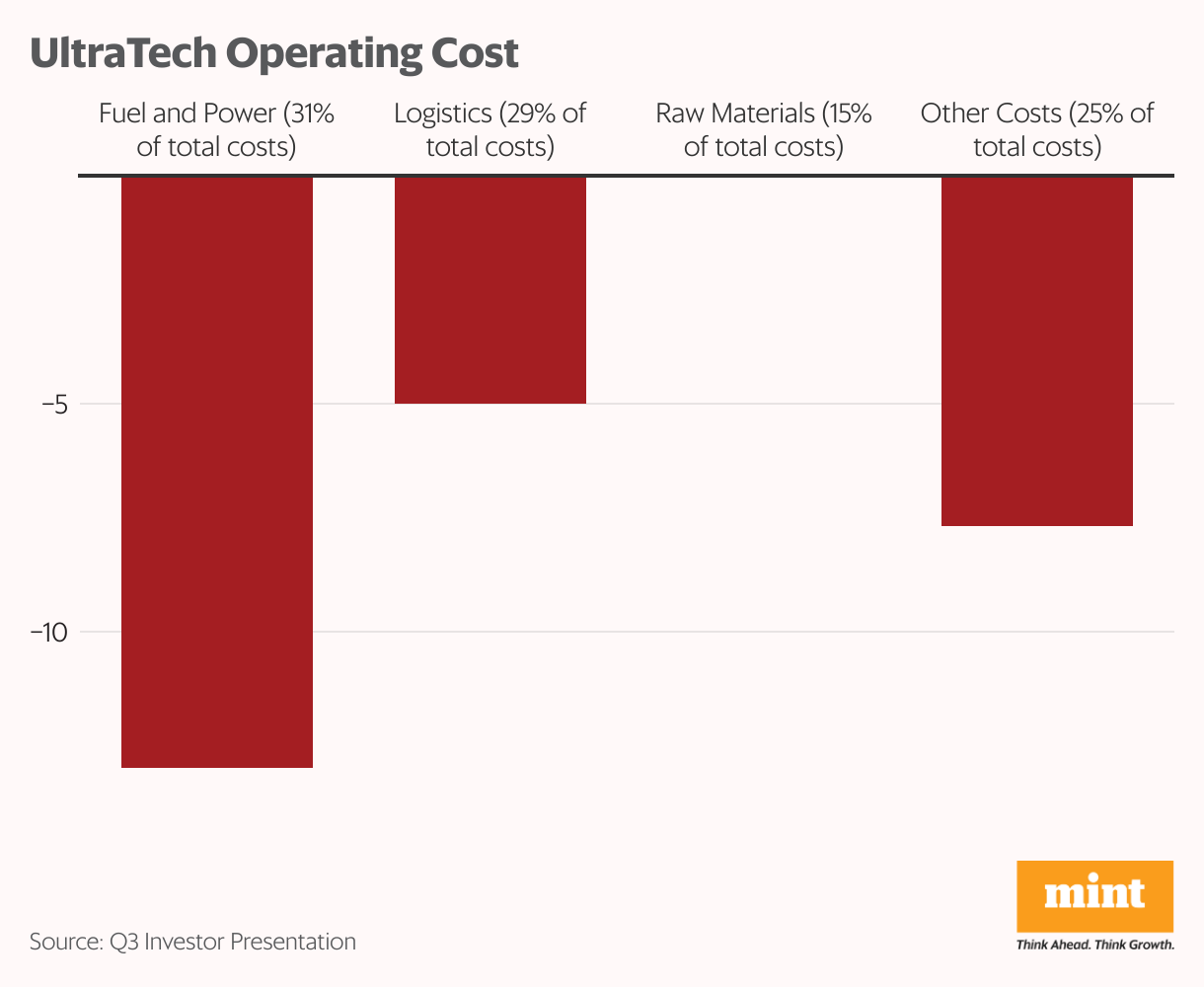

Margin pressure

In the latest quarter, operating costs eased across the board, driven by a 12.5% drop in fuel and power expenses.

Also Read : The open source Model Context Protocol was just updated — here’s why it’s a big deal

Yet, pricing pressure took a toll—realizations fell 9.6% year-on-year. While volumes rose 11%, revenue growth lagged at just 3%. Cost savings helped, but Ebitda still slipped 8%, and net profit dropped 17% to ₹1,473 crore.

Road to improvement

Sequentially, the picture looks brighter—realizations improved quarter-on-quarter, boosting Ebitda by 40%. As cement prices continue to rise, profitability is expected to improve further.

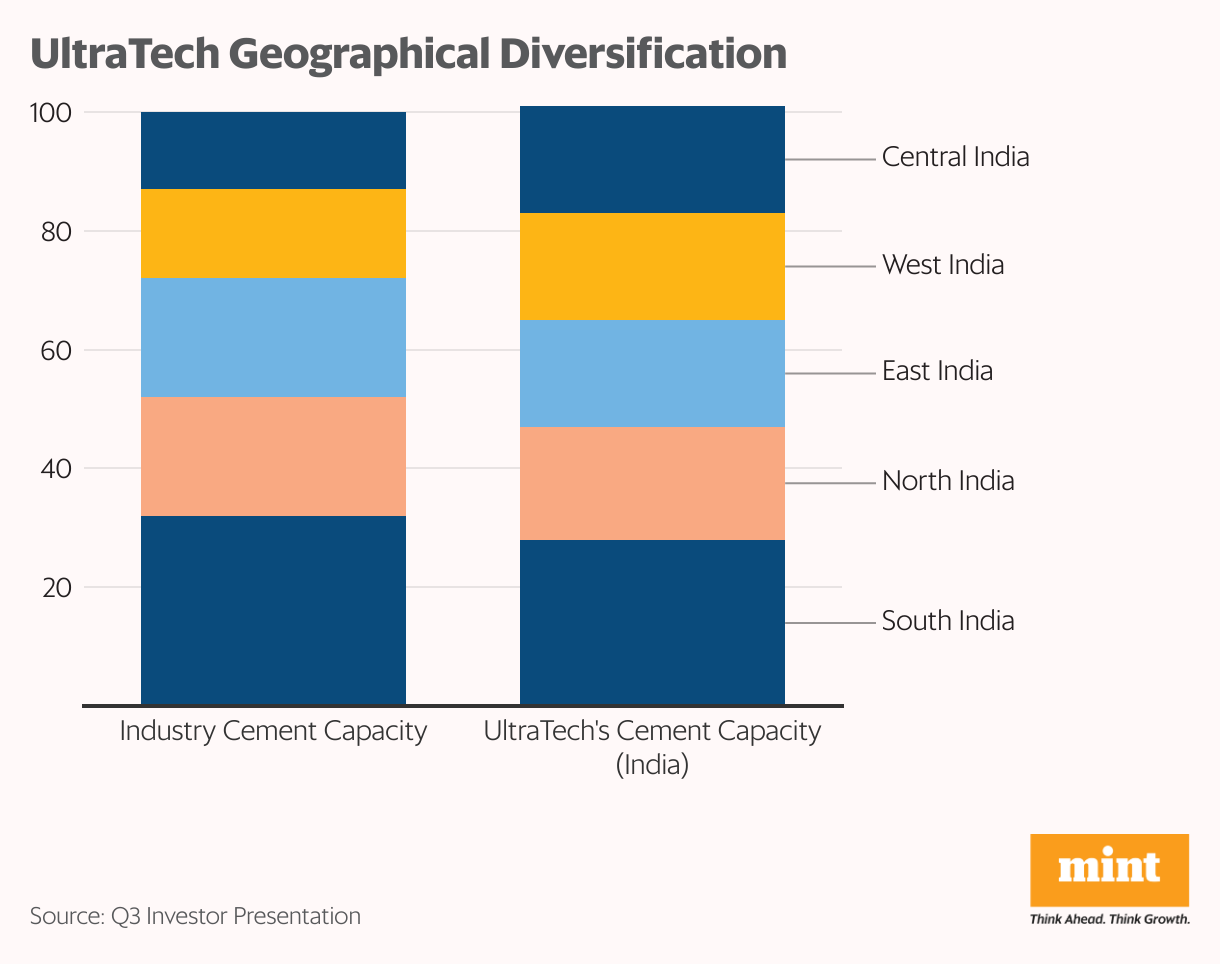

UltraTech’s geographical diversification also provides an edge. With lower exposure to the highly fragmented southern market—where pricing power is weaker—and a stronger presence in the western part of the country, which benefits from proximity to ports and lower logistics costs, the company is positioned more favourably than peers.

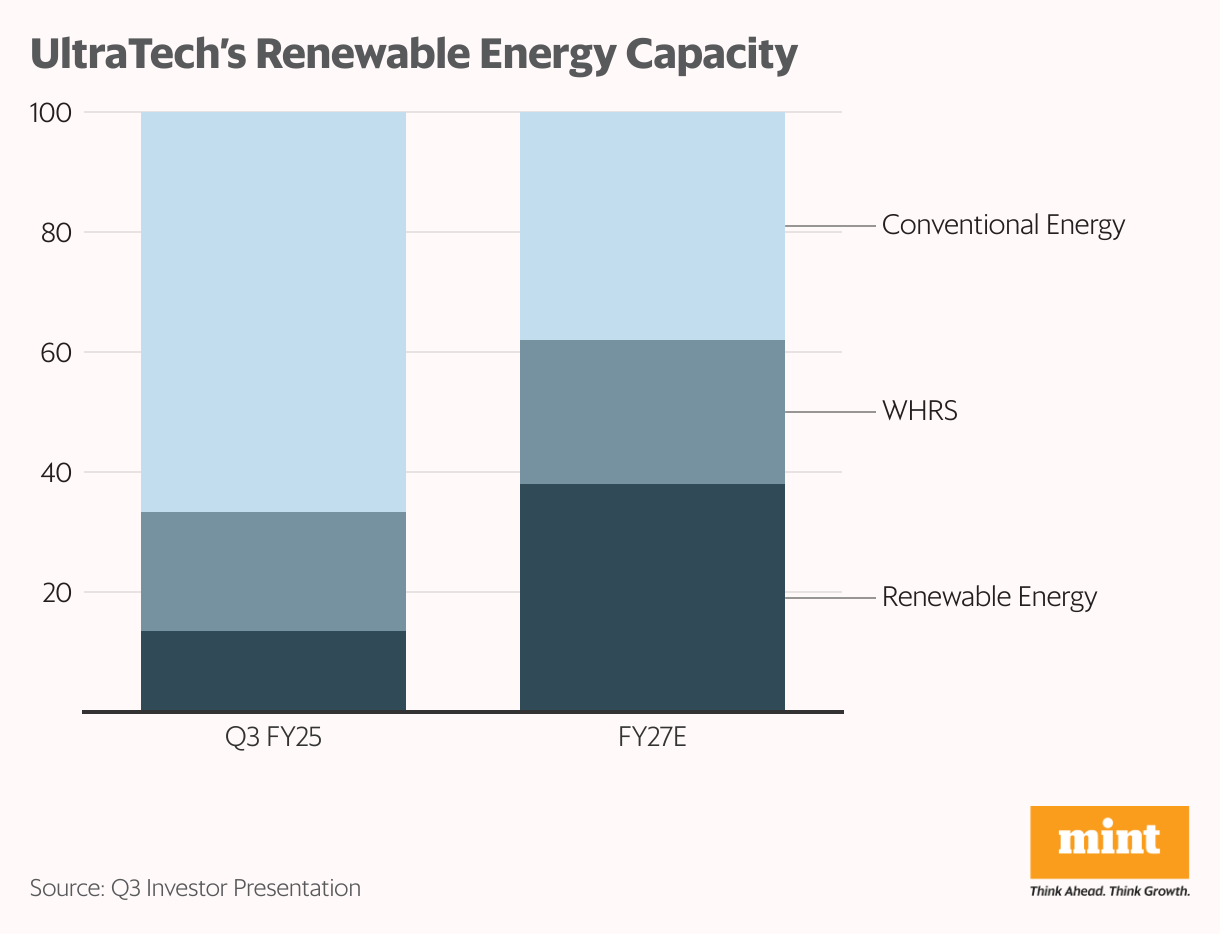

On the energy front, UltraTech is aggressively expanding its renewable capacity from 0.75 GW to 2 GW, which will meet nearly 38% of its energy needs by FY27. Waste Heat Recovery Systems (WHRS) will account for another 24%, nearly doubling the share of green power to 62% and improving cost efficiency.

Additionally, better railway logistics and synergies from acquisitions are expected to drive down freight costs. These efficiencies, coupled with the benefits of scale, are projected to reduce costs by ₹300 per tonne by FY27—an improvement over the current Ebitda per tonne of ₹960. With realizations rising, Ebitda margins are forecast to expand to 22% by FY27.

Cement remains key; C&W a long-term play

UltraTech has strategically moved into the competitive cables and wires (C&W) market, a natural extension of its core construction business. The company has earmarked ₹1,800 crore for this expansion and plans to commence manufacturing by the end of next year.

Also read | Bajaj Finserv’s insurance bet fails to impress investors

Adani Enterprises has followed suit, announcing a 50:50 joint venture with Praneetha Cables to enter the industry.

While the entry of cash-rich players with established networks poses a challenge to incumbents, gaining traction in a competitive market won’t be easy for newcomers either.

Raw material costs—dominated by copper and aluminium—account for over 70% of expenses in C&W. UltraTech’s access to cost-efficient supplies through group companies Birla Copper and Hindalco offers a structural advantage. However, initial years are likely to weigh on its consolidated performance due to higher advertising and promotional expenses, while limited scale and operational leverage could strain profitability.

With an existing debt of over ₹15,000 crore, the planned capex could reduce free cash flows by as much as 13% over the next couple of years.

UltraTech aims to achieve industry-level Ebitda margins in C&W only by FY31. The market reacted warily to this new venture, with the stock correcting nearly 8% in the two days following the announcement on 27 February, while incumbent players saw sharper declines of up to 14%.

Read this | Aditya Birla’s next big bet: Can UltraTech shake up wires & cables like Grasim did with paints?

Management moved quickly to reassure investors, stating that no additional capex would be required beyond the initial investment, pricing wars were not anticipated, and a robust return on capital employed (ROCE) of 20% was being targeted. The clarification helped restore confidence, and the stock has since rebounded.

For more such analyses, read Profit Pulse.

Meanwhile, UltraTech’s cement business remains strong, with steady growth and improving margins. UBS’ bullish stance on the company is reflected in its aggressive target price hike from ₹9,000 to ₹13,000 per share, implying a 15% upside from current levels.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment adviser. X: @ananyaroycfa

Disclosure: The author does not hold any shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.