Bajaj Auto investors get a demand reality check

Source: Live Mint

MUMBAI

:

Bajaj Auto Ltd’s shares fell 11% on Thursday after its management painted a sombre picture of domestic two-wheeler demand for the ongoing festive season while announcing the September quarter results (Q2FY25). Of course, it didn’t help that the stock’s valuations had become steeper thanks to the strong 70% gain seen until then in 2024.

While the industry expected around 5-8% on-year sales growth, actual figures till Dussehra are closer to 1-2%, similar to 2023’s performance. Even a demand revival ahead of Diwali might only lead to a 3-5% on-year sales growth during this festive season. At a time when premium motorcycles are driving most of the industry’s sales while entry-level products are languishing, a muted festive season questions the industry’s growth prospects for the entire fiscal year.

Moreover, Bajaj’s Q2 earnings before interest, taxes, depreciation, and amortization (Ebitda) at ₹2,652 crore came in lower than analysts’ expectations even though it was up 24% year-on-year. Sure, the Ebitda margin was at 20% for the fourth consecutive quarter, but can it sustain? That is the moot question.

While Bajaj plans to continue its premiumization play moving forward, its internal combustion engine (ICE) products have limited room to grow due to the existing high base of sales volume and a saturating market.

Downward pressures

Analysts from Kotak Institutional Equities believe margins have peaked out and will face downward pressures over the coming quarters due to a recovery in export volumes led by Africa (lower average selling prices and margins), a rise in the mix of electric vehicles (EV) and CNG two-wheeler segments (margin-dilutive segments), and moderation in growth for the three-wheeler segment (margin-accretive segment).

Bajaj plans to double down on the expansion of its green portfolio to create more headroom for growth. Currently, premium motorcycles—those with engine capacities of 125cc and above—drive 75% of the company’s domestic sales. The company is diversifying into CNG and electric two-wheelers. Green vehicles, including three-wheelers, accounted for 44% of its domestic revenue, to which EVs contributed around 20%.

Customer response for its newly launched Freedom 125 CNG motorcycle, the first of its kind, has been encouraging. Lower fuel cost, higher mileage and comfort-oriented product design have resonated well with a wide cohort of customers, resulting in the sale of 10,000 units in September. Bajaj plans to sell 18,000 more in October and ramp up its production capacity to 40,000 units per month by FY25.

Green push

Bajaj is also working with gas distribution companies, along with the ministry of petroleum and natural gas, to develop more CNG pumps across the country and ensure wider adoption of CNG vehicles in the coming years.

With an addressable market of around 500,000 mileage-conscious customers, Bajaj is already catering to 95% of the CNG market with around 500 dealerships across 350 towns, the company’s management said in its Q2 earnings call. Hence, it has a first-mover advantage in the CNG market in terms of product pricing and scaling of operations.

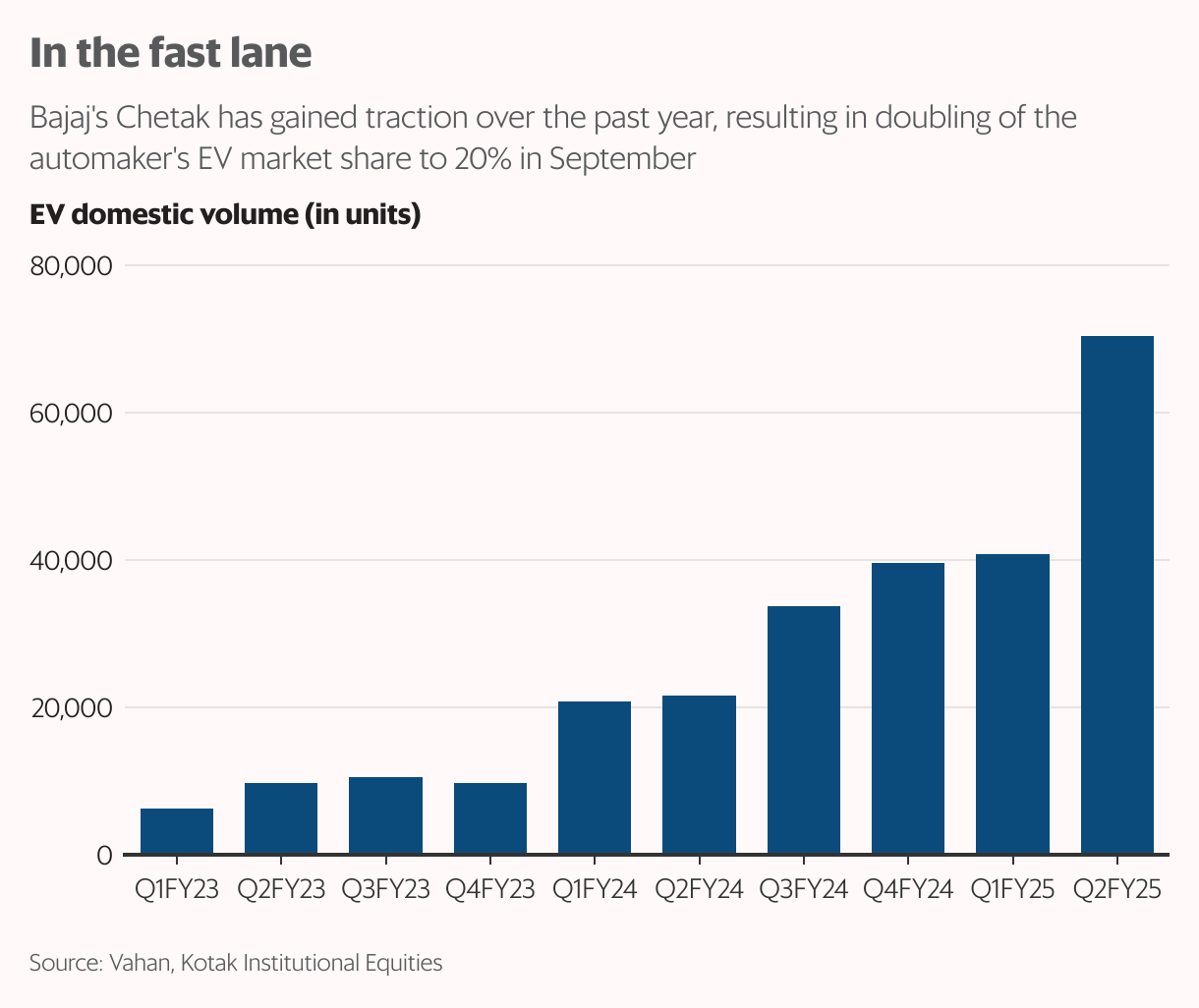

The automaker has also doubled its market share in the electric two-wheeler segment to 21% in September in just a year, indicating a strong traction for its electric scooter brand Chetak. While Bajaj is still making losses on Chetak, it plans to launch newer cost-efficient models of the scooter from mid-November.

Based on Bajaj’s strategy, Nuvama Institutional Equities has projected a whopping 43% compound annual growth rate for its EV portfolio over FY24-27.

Be that as it may, in the near term, weakness in the domestic two-wheeler market could weigh on Bajaj’s financial performance, thus capping the huge appreciation in the stock.